Time to reveal my first investment in a truly Japanese company (that is bought with Yen and only listed in Japan). What really triggered me to pull the gun was the significant JPY weakening we have seen lately, with only domestic sales I’m fully exposed to the Yen in this holding, let’s dig into Anicom Holdings!

Elevator Pitch

Dominant insurance company in it’s niche of pet insurance in Japan (estimated 44% market share).

Strong growth: 10 year Revenue CAGR of 14% and 5 year of 6%.

Founder led with CEO who still holds about 8% of outstanding shares.

Core of the thesis is really about Japanese mindset change of the role the pet has in the family. This will over time increase insurance penetration.

Moat built from highest coverage of direct settlement of bill at veterinary as well as regulatory barriers for insurance companies.

Pet industry in Japan

Anicom has been responsible for much of the growth in the Japanese pet insurance market over the years, however there are still relatively few pets covered by insurance at this time. According to figures from a 2020 Japan Pet Food Association survey of dog and cat ownership, there are roughly 18.1mn dogs and cats kept by Japanese households as pets, and only about 12% of these are covered by insurance. The UK has 16.5mn dogs and cats (8.5mn dogs, 8mn cats; about 25% of the human population in 2017) but pet insurance covers more than 25% of UK pets. So adjusted for population, UK has about twice as many pets and twice as high rates of insured pets. If Japan overtime would reach UKs level of number of pets as well as insurance penetration that is a four fold increase of the market.

As you will see below, the number of pets owned in Japan is in a rather steady state (dogs decreasing, cats increasing). Considering that the population has decreased with a few percent in this timeframe and will continue to do so, is a natural headwind. As a tailwind is that interest in pet ownership is up, but somewhat held back by the supply of especially dogs. There is a more interesting story than the steady state of pet ownership and that is around the mindset of the owners. As you also can see below the industry keeps growing in size although number of pets is not growing. We can only attribute this to the changing mindset around pet ownership. More and more pet owners puts the pet in a family position, where no costs are spared for the pet to have a good life. As a US pet insurance CEO put it: In the past 20 years pets have moved from the backyard to inside the house, and now they are moving from the house into the bedroom and even on to the bed. Press to read more..

It’s been difficult six months to try to find somewhere to hide, I have taken some hits but managed to navigate the downturn decently well.

My portfolio detracted -11% in the first half of 2022 vs -20% for my main benchmark MSCI World Total Return, both denominated in USD. Never fun to be down, but after a very weak 2021 I’m of course pleased to finally stay ahead of the index. I have talked a lot about the US market and the USD in the past. Being underweight the US market has for a very long time been a big mistake. This is probably the first half year in a long time when its been positive. The USD itself feels like one of the main macro factors to mention for this period as many compare their returns in their local currencies, which of course comes out favorably if one compares returns in a currency that lost a lot to the dollar. The USD is just insanely strong right now, this has been a big detractor for some of my investments denominated in Swedish Krona, Polish Zloty and Euro.

Returns for first half 2022

Below is the returns for my holdings during 2022 and the ending weights (not including dividends). For example Swedish Match has been a larger position but has been sold down over the past months and Modern Dental has been increased after it already fell. My position sizing and buying/selling has had a major positive contribution to the outcome.

Returns since inception

Quick comment on each holding

There is a lot to say about this half year in terms of Macro etc, but I will try to keep it as brief as possible with some thoughts on all my holdings. I hate to be so non-humble but my “everything is a bubble post” from January this year was timed almost perfectly for the start of the downturn. Ok bragging over, press more and read all thoughts on my holdings:

It is not every day your largest position get a takeover offer at 40% premium. Surely something to be celebrated – or?

Philip Morris International Inc. (“PMI”), has today announced a public cash offer to Swedish Match’s shareholders, offering SEK 106 per Swedish Match share in cash.

Fantastic for my more than slightly bruised portfolio to get a quick win but long term is this what I want?

A look in the rear-view mirror

Swedish Match (SWMA) entered the portfolio in August 2017 at a fairly modest position size, this is what it looked like back then:

Portfolio in October 2017 when Swedish Match was a new position

Over the years I have slowly doubled my initial position. Although the stock has been a good performer, for a long time my average portfolio actually did better. The difference has been that most other winners have over the year left the portfolio, but Swedish Match always stayed. Only Nagacorp has been there longer. I have been so impressed with how ZYN developed in the US and the defensive characteristics of the company. With that I was happy to keep this as a high conviction position, especially into a overheated market (as I strongly argued in my recent everything is a bubble post). With the money from selling my RaySearch shares, I luckily even re-allocated a little bit of that to Swedish Match just a few weeks back. With the additions over the years, and strong stock performance Swedish Match was my largest holding when the takeover offer came in this week. My portfolio as of Friday (before the offer).

Portfolio as of May 6th 2022

I have a decision to make

Like all shareholders I have a decision to make:

Sell my shares now, trading at roughly 103.5. In this price there is the risk that the deal breaks which would then be mitigated, I get something guaranteed very close to the offer. But selling at this price also foregoes all call options that the bid would be increased, or another bidder would come in to challenge PMI.

Wait and accept the offer, that implies a nice cash yield of 2.4% until the money arrives in September. One could argue that I should then even increase my position and put my cash in Swedish Match for a nice yield on cash. That is if I believe there is zero risk that the bid is withdrawn. I would then also enjoy the upside potential that there would be a bidding war.

Not accept the offer. I come to the conclusion that this is a stink bid and Swedish Match is actually worth more. My hope then is basically enough other investors come to the same conclusion and PMI either fully takes back the offer or buys a so small part (could still be majority owner) so the company stays listed. This is tricky in many ways, because if PMI becomes a majority owner and I’m left with shares in something that now is fairly illiquid and the majority owner wants me out. It could be a long bumpy ride, perhaps something I’m willing to do with a normal sized position but it would be hard with my absolutely largest holding (consider the 12.8% weight above is pre-offer). This makes me conclude there is a 4th option:

Reduce position size (take partial profit) and not accept offer with smaller position.

Attacking the above one by one:

1. Sell my shares now

In fact I have already sold about 8% of my position on Monday to slightly de-risk, this was before the bid level was confirmed. Further than this I’m not considering this option anymore. I see it as highly unlikely that the offer fully falls through.

2. Wait and accept the offer

For the time being I’m definitely waiting, I think there is a small chance that a competitor or even VC/PE fund will come in with a bid. As as another bid is that a lot of larger shareholders would be in talks with PMI over the coming months, making them understand that the offer will not go through on this level. PMI would then be inclined to increase the offer.

3. Not accept the offer

Even if this is not a stink bid, it’s actually not far from it, why? Because the SEK is weak as hell against the USD now and the bid is in SEK whereas the attractive parts of the business they are buying is USD based sales in USA. The refer to the 40% premium to the share price but this is not at all the case from a USD investors perspective, as I am and PMI are as well.

As you can see from the above graph, if investors were happy with the offer valuation, we had plenty of opportunity to jump off at price levels close to this price during last year. But OK, markets are down since then so surely one can’t expect ATH levels and then a premium on top of that. Well yes you kind of can, because SWMA was not a stock that participated in the growth hype category. This was a stock that was very unloved, who wanted to own a tobacco company in these past years – well basically nobody.

Looking at it from a valuation perspective it looks even worse, since the company keeps perform well. The bid is basically at a mid valuation over the past years. This graph was actually the reason I added to the stock just a few weeks ago, it felt very defensive and trading close to its 10 year lows in terms of EV/EBITDA multiple.

4. Reduce position size and not accept offer with smaller position

Given how tricky this situation is, getting potentially caught in a less liquid stock among a smaller group of disgruntled investors with PMI perhaps owning 60-70% of the shares, the best option might be the last one. De-risk a bit, celebrate the nice gains but actually keep a decent position waiting to be actually properly paid. And what is properly paid then? Well given the synergy values this has for PMI, arguable SWMA should have a higher value than it has for the general market. Given that we historically traded at 19X EV/EBITDA, I would say 20X EV/EBITDA is some type of minimum for not being called a stink bid. Which would imply about 25% higher offer than the current value, so in the range of 130 SEK per share if you use a forward looking EBITDA estimate.

For an actual really attractive premium which I believe most would agree is fair and good we are talking 150 SEK per share. That feels highly unlikely though given the 106 SEK they are offering now, so perhaps if more people feel like me, this bid will actually not be successful after all.

Others do agree its a stink bid

John at Bronte who was kind enough a number of years ago explain his deep insights on the company, does definitely seem to think its a stink bid.

Hearing from other informal sources other professional investors do feel the same as John.

That said there are also big players like Capital, who own 10% of SWMA and are large owners also in PMI, given them sitting on dual shares one would guess they are inclined to agree to the offer. It’s a tricky situation indeed.

Conclusion

For the time being I’m keeping my shares, hoping for a better offer. If no such offer comes I might sell some shares close to the offer deadline and probably keep some fighting for a better price together with John and others. All of this could of course change given what the market does. If the market falls 30% in the next few months, this offer will relatively look better and vice versa if markets rally from here. Finally SWMA presented their latest report today and it was incredible to see how they just keep growing and even taking market share with ZYN in the US. This picture gives a pretty nice sneak peek of how Total US could develop over the coming 3 years.

Disclaimer: This post is for general information purposes only and does not constitute investment advice. Always do your own due diligence. Please see full disclaimer on globalstockpicking.com.

Elevator pitch

Only independent software company in radiotherapy for cancer treatment with very strong product offering, never lost a customer.

Founder led company which spent more on software R&D than the current market cap of the company.

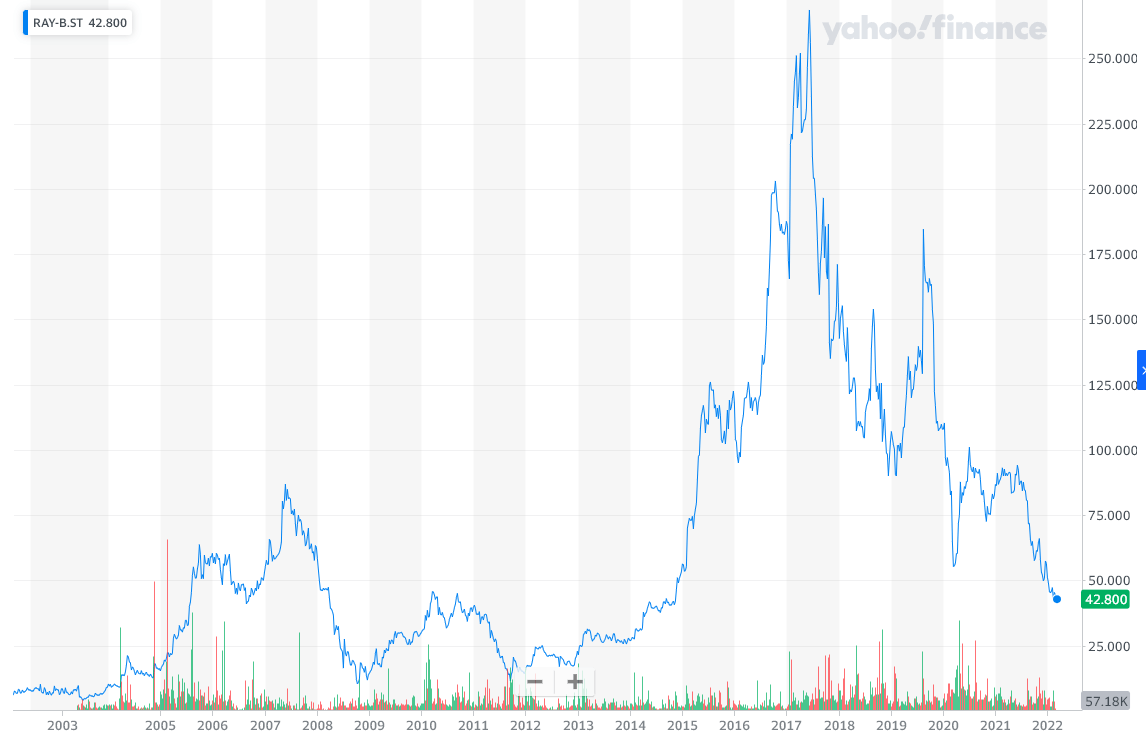

Although their product is good, a strong R&D push which reduced profits + previous aggressive accounting and now Covid-19 has hammered the stock from 260 to 45 SEK.

New CFO in place and CEO/CFO has promised focus on cost control (for the first time).

With a stronger software offering, hospitals are going back to business as usual, latest report confirmed early signs of turn-around.

RaySearch has 70% market share in proton therapy, which has a very strong outlook the coming ten years.

With very conservative estimates more than 60% upside and a weighted valuation pricing gives 85% upside.

Background

RaySearch is a Swedish medical technology company that develops software to improve cancer treatments. RaySearch software is today used by over 2,600 clinics in more than 65 countries. The company was founded in 2000 by Johan Löf as he was working on his PhD in radiation treatment. Johan is still the majority shareholder and CEO and has proudly stated that RaySearch has never lost a customer, that’s a pretty strong statement.

In the early days RaySearch delivered functionality to the leading treatment system vendor Philips. In 2003 RaySearch listed on the Stockholm exchange. RaySearch is developing highly complicated software in a very specialized field. The cancer treatment facilities are among the most complex areas in a hospital and requires both very advanced machines and software. Radiotherapy kills the cancer cells by various kind of high energy beams, like x-ray or protons. The core of RaySearch products and what Johan worked on already in his PhD is a more clever dosing of the dangerous radiotherapy. Basically “burn” away the cancer with higher precision, meaning minimizing damage to healthy tissue. After the early cooperation with Philips, RaySearch tied more and more partners to its development. Companies like IBA Dosimetry and Varian as well as certain large University hospitals worked together with RaySearch. Over the past two decades RaySearch grew from a small niche player with some smart algorithms into the only major stand-alone software company in this field. All this was done without any share dilution, RaySearch has funded all growth by being profitable from a very early stage. This R&D has coincidentally costed RaySearch just in line with the current Market Cap of the company (1.55bn SEK). Let’s look at the history and the products RaySearch developed in greater detail (press read more).

What does a bitcoin speculator, a Rolex collector, a Magic the gathering cards collector, a wine collector and a tech growth stock investor have in common? Not that much they might think, but in my view something happened in 2019 that got all of these people exposed to the same something.

My previous post headline claimed that my watch outperformed my stock portfolio in 2021. I thought we should dig a bit deeper into that. I think most people by now are aware that low interest rates and stimulus pumped up asset prices all over the world. Equities and bonds are at record valuations at the same time, is something we heard for quite some time now. Of course it doesn’t stop there, crypto has created tons of newly rich people. House prices have soared in most places of the world, everyone who own anything seems to have done very well for themselves. A question that at least skeptics like me keep asking is: If the world did not get much better in terms of inventions or production of goods, how is possible we all got so much wealthier? So what? Its good times and the economy is running hot, what’s new? Well not everything has run equally hot, some asset price increases have been just off the charts the past few years. That’s what I want to dig deeper into. Also in in my stock portfolio some holdings have taken off like rockets whereas others have actually decreased in value or been flattish. So we know FEDs balance sheet has shot up like crazy in the past years and we know about the super low interest rates – but what distinguishes these certain sets of assets that just sky rocket?

To cut to the chase, the short version in my view is that we created a bubble. A new kind of, everything is a bubble bubble, which is pretty unique for how bubbles goes in an historical context. Usually bubbles are concentrated in something, like tulips, tech stocks or so. I don’t literally mean that everything is in a bubble, there are plenty of things out there at reasonable valuations. I just mean its a really freaking wide-spread bubble this time cutting across assets classes and countries. Let’s go back to my watch, which outperformed my stock portfolio in 2021 (and probably in 2020 too). I thought a lot about this, not really from the context of watch prices per see, but how risky assets re-priced in the past years. I have tried to look for patterns and would like to share some of the bread crumb clues I looked at. My conclusion is that what has sky rocketed in value the past two years, they all play to the tune of the same factor. In the past they didn’t necessarily really have that much to do with each other, but in the past two years, suddenly they did.

Finding the common bubble factor

What does a bitcoin speculator, a Rolex collector, a Magic the gathering cards collector, a wine collector and a tech growth stock investor have in common? Not that much they might think, but in my view something happened in 2019 that got all of these people exposed to the same something. “Something” was driving the action in their respective holdings the past 2 years. I call in the everything is a bubble factor. Let’s take a look at how price action looked like in the past years:

So I got onto this topic when my portfolio had outperformed the market quite significantly. I noticed that there were particular holdings that had extremely strong short term performance on very little actual fundamental company change. Back then most people only talked about how value investing is long dead and so on. But it was only when I plotted this graph in mid-2020 that I understood that growth stocks had just gone into hyperdrive mode. Around the same time some twitter names started to boast extremely good portfolio performances, they had portfolios fully exposed to this factor and were now bragging about their returns. As the ever contrarian I am, I got worried I was also just surfing on this factor – and not really created any actual alpha. With hindsight I shouldn’t have worried but rather piled into this more deeply myself, because this spread just kept delivering and delivering until about three weeks ago.

Just to be clear what we are looking at above, because I find this – sick, hilarious and just bonkers all at the same time. Above is the Vanguard ETFs which replicates the CRSP US Large Cap Growth & Value Indices. Buying the Growth Index and Shorting the Value index gave you a nice 20% outperformance between 2017-2019, a very strong out-performance on index level in the same market. That was probably justified as companies like Apple, Microsoft etc did improve fundamentals quicker than for example JP Morgan, Berkshire and Pfizer (companies found in the value index). But then in 2019 all of a sudden in 2 years time the growth companies went up 100% more than the value companies. How is that possible to be even close to reasonable? In my book its not, markets ran way way ahead of themselves. Let’s look at some of the other “assets” to see if we can see a pattern between this Growth-Value spread and the rise of other assets:

Watches

With a bit of lag to the Growth-Value spread grey market prices of watches seems to take off in a very similar pattern. Look at the AP Royal oak which basically doubles in value in about 1 years time. These watches are now selling for multiples of what they cost in the store (if you are lucky enough to be allocated one). So should we be buying stocks or just hold physical portfolios full of Audemars Piguet watches? Historically these watches have been good store of value, basically rising with inflation, Rolex is famous for this over long periods of time and much of its special status is probably due to this good second hand value. But now we are talking about watch prices doubling in the span of 1-2 years, trading over 2x the retail price. Rolex produces roughly 800 000 watches per year, which are sold at retail (in some few cases the retailer might do some shenanigan’s to extract some of that grey market premium but most often not). These watches have supply constantly coming into the market but still the demand is so much larger than supply that these watches can catch such premiums. To me this is again just bonkers and typical bubble sign. So how about my watch? I did not in fact buy either a Rolex or a AP but my watch has had a similar trend as these. For the avid twitter stalker and watch enthusiast you can figure out what I got 🙂

Wines and Champagne

Again we see the second hand prices of rare wines just taking off (after flat lining for many years). It’s clear people suddenly got so much more disposable income and everything went into scarcity as people bid up prices rapidly. Although the scale here is not like other assets a double or triple just a “meek” 30% increase, its still pretty significant for somethings so large as the average prices of the whole worlds stock of fine wines.

Magic the gathering cards

One of my person favorites, collector cards from MTG. I still have my collection in my parents home, just like the price of the most famous card in the picture here, the Black Lotus, my collection has roughly tripled in value over the past 2 years. My parents who are very frugal do not really have anything expensive in their home. Somehow my mom anyway got a bit irritated when I messaged her and said that box of cards tucked in away in one of the wardrobes is probably the most valuable item they have in their home. Just wanted to give a small FYI reminder to be careful with them but that was apparently insensitive saying they didn’t have anything of higher value than my Magic cards – sorry mom!

Bitcoin

And finally “everyone’s” favorite asset class over the past years, for extra clarity I merged the graph with my Growth – Value spread:

The trend is so clear so no further arguments are really needed, this spread and bitcoin trade on the same factor – the bubble factor.

Why bubble?

So why do I say bubble factor? It’s because its impossible that things so very different like Rolexes, Magic cards, fine wines and bitcoin all have something so fundamentally in common that they should all reprice to multiples of what they traded on before at the same time. There must be an underlying frenzy/inflation or similar driving these gains. And although we have seen inflation it has not been anything near these levels of gains. Many of these assets like Rolex, Magic cards and fine wines, have 20+ years of price history showing very stable pricing, how is it possible that they all should reprice at the same time? It’s very clear to me that the combination of stimulus money and sitting at home locked down through Covid measures created this momentum frenzy into all kinds of assets. This fed on itself and prices on pure momentum/FOMO continued to move higher. As all bubbles unfortunately they always come to an end..

This is the Growth – Value spread over the past 3 months, I wonder how second hand watches will perform the coming year? 🙂

There is no beating around the bush on this one, 2021 unfortunately was a lost year for the GSP portfolio. I bought a watch in mid 2021, it has already appreciated with roughly 10%, easily beating my 2021 performance of 3% return. That a watch can out-perform my portfolio is a pretty humbling experience but also nicely summarizes how upside down the world has been in later parts of 2020 and 2021. I have very mixed feelings about my 3% return for the year. I’m proud of how I covered stocks nobody else looked at, for example Modern Dental which is up +286% this year and I took profits when it was up 600% on the year. It’s pretty head-scratching then to have achieved such home runs and only be up 3% overall. The explanation is of course that broad parts of my (China/Hong Kong related) portfolio has just been hammered. So I will spend at least a bit of time harping about how incredible the spread is between Hong Kong and USA listed stocks in 2021. As you can see in the graph below, MSCI World excluding USA is on a total different trajectory. Since I barely invest in US listed companies I look like a terrible investor not because of stock picking, but because I have not been allocating to US stocks – rough! I do have exposure to other countries like Sweden/Finland/Poland, but even they failed me this year except one bright spot – Irisity. There I can’t blame having bad Beta exposure, I just didn’t pick the right stocks.

+

Given the low correlation (43%) to MSCI World is it still fair to use this as my benchmark? For 2020 that correlation was 87%.

Portfolio changes

Some highlight below in terms of good & bad decisions for the portfolio in 2021

The mistakes

AK Medical

I had initially bought the stock at 4.7 HKD in 2019 and quickly sold out around the 9 HKD level as the stock surged. The company continued to post great results and with multiple expansion on top of that it peaked at 26 HKD. The stock after that started a major down move due to fears of the changes in Chinas central purchasing of medical equipment and devices. I tried to look into the topic and as I understood it it would mostly be the distributors taking the hit and not AK Medical. I still believed in the long term story of aging population with higher disposable income, there will be a huge need for knee and hip operations in the coming 10 years in China. On top of that China is getting more nationalistic, surely they want the market leading local player to have a pole position here? I started the year by taking a position again in AK Medical at 14,7 HKD and a few months later doubled my position at 9.7 HKD. How the central purchasing actually pans out is still unknown, but for now it seems the market has agreed upon that it will be brutal. The stock ended the year at 6.6 HKD, -46% from my average purchase price. I’m slightly shell shocked by this move down, the market is basically saying that nobody will make serious money on hip and knee replacements in China, although China is one of the worlds largest markets. I can’t really believe that will be the case but the market doesn’t really agree with me. In my view AK Medical has good enough products to even shift focus to selling their devices abroad, which they already do in smaller scale. I will stubbornly keep this holding for now but not add until I see some proof of where this is heading. Market has already priced in a disaster, so I will only sell on proof of disaster.

Valneva

It was a pretty lucky stroke to research vaccine producers in 2019, 3 months before Covid started. Given that I did so, one might say I should have bought Moderna, which I never did. I am very happy though that I did buy Valneva and what a ride it was. I first purchased the stock at the very end of 2019 at 2.57 EUR, I then sold in Feb 2020 at 3.4 EUR (this was all still non-covid related). In May 2020 they announced their partnership with Pfizer for Lyme diseases, I also had a small hope that they could somehow get involved in Covid vaccine production. So I took a position again, unfortunately smaller than my original position at 3.98 EUR. I rode this and sold this at an average of some 14 EUR in February 2021. Given how Covid has developed, this was like the other vaccine makers something to hold on to, its now trading at 19 EUR per share (very volatile in the past days). It felt good when I sold but it would have been a good portfolio hedge to keep.

Alibaba

Another disaster decision was trying to buy the dip in Alibaba. I mean its not really even my style to invest in large caps, I have concluded many times I have no edge in these large cap stocks. So I feel double the fool when I dip my toe into one of these mega-caps and manage to catch the largest wealth destructor ever in a single year. I bought shares in May at 214 USD and increased my position in late September at 147 USD. Stock ended the year at 119 USD.

The right moves

Modern Dental Group

My shining star investment in 2021 which I already mentioned, was ironically on the Hong Kong exchange. In this weak market find a winner makes it so much more extreme. I sold most of my Modern Dental in the bottom of the Covid crash 2020 at 1.14 HKD. The reason was because I realized that dental clinics would be shut down and indeed they were. I kept a small position because I still believed in the company long term. As soon as the positive profit alert came showing that the business had rebounded I re-entered with all shares that I sold at 1.84 HKD. That turned out to be fantastic timing as the stock just sky-rocketed basically from that day onwards. I took some profits at 5.2 HKD as the stock grew into one of my largest positions and then cut again at 9.4 HKD as it again grew to one of my largest positions. Around these levels I felt the stock had gotten ahead of itself just momentum speculators pushing it past fair value. Today it’s trading at 5.54 HKD and business seems to continue to perform very well. I do think I found a potential gem to hold in the portfolio for the long term here. The stock is just barely up from its IPO price in 2015, revenues have doubled and profits more than tripled since then. It is still not an expensive stock and just today I actually added a little bit.

Essex Biotech

This was a serious laggard in the market early this year and I wrote a blog post in February 2021: Essex Biotech – Why I am bullish. I increased my position at 3.95 HKD. The stock then went on to almost double from there on back of good results and a strong Hong Kong stock market. For portfolio balancing reasons I took a small profit in July at 7 HKD. This turned out to be fantastic timing as the stock has been pulled down heavily by the weak Hong Kong sentiment, ending the year at 4.95 HKD. Fundamentally the company still seems to be on the right track and I’m looking forward to if the company can finally get a breakthrough with the wet-AMD (eye disease) trials they are funding through listed company Henlius.

JOYY

What a mess this stock has been, its almost painful to write about. Baidu wanted to buy JOYYs Mainland business, a short report was released that targeted the mainland business. Left was a fairly attractive international Videochat business called Bigo Live. Baidu seemed happy to go through the with the deal, shooting down the short case for the stock. I believed them and added to my position since the cash from Baidu + other cash was as much as the market cap of the company. This was at 119 USD per share, my previous shares were bought at 64 USD. I capitulated when the deal finally seemed to be falling through when stock was at 55 USD, its now trading at 45 USD. So short term it was the right decision to sell but to be honest it still feels bad to have sold at these levels. Finally why I actually did sell was because I did track the Bigo Live app a lot myself (meaning I used it) and I could see that the popularity with the app was dying, basically negative momentum when they should have had positive momentum. Since I sold and it continued down I put this in good decisions (for now).

Other worthy mentions

Pax Global

This didn’t really feel like a mistake on my side, but a very very freaky event. In the middle of the Hong Kong stock market weakness, when PAX was one of few holdings to still trade close to all time highs, the nightmare news were released. FBI was raiding PAX warehouse in the USA on alleged security concerns with their payment terminals. The customer which alerted FBI had also decided to stop using PAX devices, stock was down some -45% in one day and this was before the drop my largest position – what a nightmare. Now the dust hasn’t fully settled on this but some of PAXs largest purchasers have come out and defended PAX saying they don’t see anything wrong with the devices. One could argue that is in their interest since they probably don’t want to recall millions of payment devices. Adding to this PAX still operates in USA, FBI or any other agency has not banned them from the US market, so it does not seem they so far has found anything. Lastly PAX has hired a large famous US security firm to independently check their devices (Unit 42 by Palo Alto Networks). The results from this was: “Unit 42 reported that the network traffic reviewed was consistent with the intended features of the associated services of PAX terminals. Unit 42 also concluded that there were no unexplained network traffic in the course of its comprehensive and thorough inspection.“. I don’t think PAX actually can do much more, some confidence in the company has been lost for sure both from investors but more importantly the distributors and purchasers of their devices. How much will these large buyers in Brazil/India and elsewhere shift to other brands to avoid PAX due to this? Well that’s basically what the market has taken a view on here. The market is basically pricing zero to very low growth, meaning that a major shift to competitors will happen over the coming years, I think that is exaggerated and there must be good reasons why they choose PAX in the first place (pricing vs competition, Android capabilities, PAX app store etc). I’m betting that this will slightly affect growth but PAX will still be growing at +10% or more per year. I slightly added to my position today.

Nagacorp

Another big loser for 2021, but here it’s in my view actually warranted. Given how China continues to be closed down and the funding risk of completing the Naga3 construction it’s pretty fair Nagacorp has traded down as it has. Given this view, this is where I found some of my funds (except the small cash buffer I had) to fund my purchases in Modern Dental and PAX. I haven’t sold all of my Nagacorp, but I reduced this to a smaller position today. I think the company could bounce back majorly in 2023 but Asia is still far behind on moving on from Covid.

That’s a wrap for my 2021 review. In my next post I will dive a little bit deeper into why my watch outperformed my stock portfolio in 2021. Because it has really been a year where all assets went up (except my stock portfolio and a few poor other bag holders who invested in Hong Kong) 🙂

+ Exchange business are attractive both for their moat and resilience in an inflationary environment.

+ GPW is trading a highly attractive valuation where even a bear case gives upside in share price.

+ Attractive dividend yield north of 5%.

+ Polish stock markets have not seen the rally developed markets have, perhaps the best is yet to come?

– Poland is politically moving in a worrying direction and GPW is majority own by the state.

– Although revenue has increased nicely in the past 10 years, net income has not expanded as much.

First, thank you all for the warm words in the comment section, it’s good to be back! The inflation debate is still raging, transitory or not, at least temporarily it is a reality. Some companies are really hurt by inflation, struggling to pass on the cost, others do better. I put quite a lot of thought into what companies except banks do well in a high(er) inflation environment? I came to the conclusion that stock exchanges with reasonable current valuations (not priced for too much growth) could be a sweet spot. The hunt started and I quickly honed in on the Polish exchange – GPW. A lot of listed exchanges has re-rated in the past 5 years, many driven by the strong local equity markets, buyouts etc. Others, like Hong Kong Exchange have benefited from the US/China conflicts with Chinese companies opting to list in Hong Kong. But Poland has not seen a proper equity bull market for a very long time, valuations are still very reasonable in general and the country and its savings/pension mechanism are in early days. So the days in the sun for the Polish exchange seems to still lie in the future. Let’s dig into what the company is about and if it’s something for our portfolios.

History

The Warsaw stock exchange held its first trading session on April 16, 1991 with five listed companies, all of which were formerly State-owned companies that had been privatized. In 1999, Poland reformed its pension system, which contributed to an increase in domestic institutional investment, and in 2004 it joined the EU. With a record high growth in EU over the past 20 years, all these developments helped to boost trading volume on the exchange. In 2010 Giełda Papierów Wartościowych w Warszawie (GPW) listed on its own exchange.

Through my other Polish holdings I have written about how Poland is one of Europe’s strongest growing markets. On the back of such growth naturally a large population like Poland is creating national champions. Two worthy mentions would be CD Projekt (18bn PLN) and Allegro (71bn PLN) which recently listed. Overall the Polish equity market is very strong in gaming companies with many smaller players listed. GPW has also successfully developed a commodities exchange over the past 10 years. Today the commodities segment revenue is as large as the Equity/Fixed Income trading segment. To summarize on the back of Poland’s growth, so has also the exchange grown. That said, GPW is still tiny compared to developed markets with a market cap of 430m USD. Being in such an early stage of development I see plenty of long term growth opportunities for Poland and the exchange.

Company Overview

To get a better grasp of the company the below picture gives a good overview of how revenue is generated (press to read more):

Back in May-June after my last blog post my life and portfolio was in bloom, I had my best outperformance since the blog started and I was back good physical shape. That did unfortunately not last and things went quite wrong from there on. I had struggled with my health for the past year and early this summer it got worse than ever when a injured myself quite badly. I’m much better now but going through something like this really drain you. Currently going through the slow process of trying to build up strength again. Due to these unfortunate health issues I haven’t had the mental capacity to post anything or research as much as I used to. But now after exactly 4 months of inactivity I’m back blogging. I got a bit of a writers block starting off this post, I try to just come as you are. Nevermind my health issues, let’s put focus back on what happened this summer and especially China.

Having a strongly China tilted portfolio has really been bad beta exposure these past months, the spread between developed markets and Hong Kong is really remarkable. Just like health issues which sooner or later emerge, I knew the day would come when China would have to clean up its imbalances and go through a readjustment/bust. I read plenty of books on the topic and spent considerable time trying to understand the dynamics of for example the Chinese housing market. Being somewhat mentally prepared and thinking through the downside helps, but it still hurts when it happens. My portfolio has taken it on the chin lately, but perhaps not as bad as one would expect. I had such a tremendous run in some of my holdings previously, that gave me plenty of cushion. Also I have had minimal exposure to all the sectors that have been worst hit. As of last Friday my portfolio is now in-line with MSCI World (20% vs 18%) and massively ahead of Hang Seng (-8%) YTD.

Portfolio changes/comments

Modern Dental Group

Although I haven’t posted I have stayed somewhat active in the market. I had to, for example Modern Dental continued to double yet again from where I started to reduce my position. I was very happy to unload another portion of shares at 9.4 HKD, keeping half of my initial position for the long term. This stock alone saved a lot of my bacon in terms of performance this year.

Greatview Aseptic / Vinda

I have been gradually increasing my position size in Greatview Aseptic, which I think is underappreciated and undervalued here. Yes the semi-annual was a bit weak in terms of revenue falling down to the bottom line, but revenue grew nicely YoY. Given the increased raw materials prices and the extremely stretched transportation market it was no surprise to me that profit wise it would be a somewhat softer half year. This is still a growth company (growing revenue some 9% YoY in the past 4 years) with a 8-9% dividend yield, priced as a zero growth company. Doesn’t make any sense, so I will continue to back up the truck and load up more. I added shares at 3.74 and 3.45 HKD, which apparently was too early as its now trading below 3 HKD.

In the same manner Vinda has come down in valuation, I added some shares at 23 HKD, again not the best timing but quite happy to add shares at this level. Both of these companies have similar characteristics: totally unsexy business, factories producing daily necessities, founder led and both taking market share in a market with a tailwind. This means the can post high single digit growth rates, which is nothing to scoff at in the long run.

Pax Global / Essex Biotech

Did some profit taking in both to fund the additions in above mentioned stocks, here I sold at good levels, 9.76 and 7 HKD per share. The selling has not really anything to do with not believing in these companies (they are even after selling my largest positions), just that I want to balance the portfolio and re-allocate to for example Greatview which I see as having better return potential from this point.

Dream International

When I added this company to my portfolio I wrote this post, with the question mark a dream Investment? I wouldn’t say it turned into a nightmare, but not far from it. I bought at 4.11 HKD and sold out 3 years later at 2.88 HKD, throw in a couple of dividends of some total 40 cents or so and its still a handsome loss, during a period my portfolio almost doubled. Incredibly enough most of the loss comes from the EV/EBITDA multiple contracting from 5 to 4, cheap got even cheaper. It’s ridiculous to sell but also ridiculous to allocate capital to something where shareholder value never seems to unlock. It would be painful to see the company announcing a special div or something like that now and the stock doubles, which would be reasonable. Such is life in value investing land, some stocks are just to deep value traps and this one I throw in the towel on. I could write tons more about this company, but choose to cut it short since its no longer in the portfolio.

Irisity

I have been flip flopping a bit in Irisity. I reduced my position in July thinking the odds for a continued rally seemed weak. Then they announced a merger with an Israeli company in the same sector, basically removing a one of the largest competitors (not that any of these players are large) and maybe more importantly gained a decent sales force. I think building some scale into this company is really needed and I saw this move as worthwhile to put on a position again, which I did a few SEK higher than where I sold 58 vs 61 SEK per share.

Nagacorp

Oh boy this has become a tricky one. The share price has taken a proper tumble dropping more than 50% from ATH. The market seems to focus more on the short term pain of Covid and Casino closure than the possible long term gains. Here you can see the sentiment difference between for example the US cruise liners like Royal Caribbean which has fully recovered from its Covid drop, although cruise sales worldwide has not fully returned. In this cases the market was quick to take the long term view but in Nagacorp’s case the market is either short sighted or changed its view significantly on future income potential. My interpretation of what the market thinks, its a bit of both. Short term scared that it could still take years for Cambodia and Asian markets to resume travel, combined with what has been happening in China with new rules for Casino Junkets, which makes it likely VIP business will not come back as before. This double uncertainty has just killed the stock. On top of that there is also some overhang fears of how the funding of Naga3.

I decided to add to Nagacorp (again too early) in July at 6.98 HKD per share. My reasoning being that Cambodia is a friend of China, which can be seen by high vaccination rates they got compared to the rest of south east Asia. My guess is that Cambodia will be one of the first countries which will open some type of travel towards China. But say I’m wrong and travel does not resume say in another 2 years, then the situation is tricky. Naga3 will be delayed and probably cost more to finalize, the down period will then be so long that I think share dilution etc will be a fact. Nagacorp will turn into a disaster investment with permanent loss vs current limbo situation. In my view all of South East Asia can not afford to be closed for another 2 years, yes it would crush Naga as an investment case but it would crush the economies of these countries more. Still I’m humble to the possibility of being wrong and I don’t want to size my bet too big, I’m not going to add further (7% position) until I see signs of actual improvement. In regards to VIP business, yet to see where this lands, I have a small hope that junkets will be more controlled in Macau but will find ways to continue to operate in Cambodia, but my base case is that VIP does only come back to 60-70% of previous levels, which is still good. In other words in my view risk reward looks good, but outcomes could be extreme both on up and downside.

New holding – GPW SA

A third Polish holding enters the Portfolio, the Warsaw stock exchange itself, a separate post will come soon!

China

A few words on China specifically as well, given all the things that happened perhaps I should dedicate a separate post to it. Since I started this blog I always had mixed feelings about my tilt towards HK listed companies and China exposure. First time I got bearish on the blog was 2017: Rotate away from China. Already back then I spelled out my worries of China property and sold out of my holding Ping An. Ping An has lately been one of the largest indirect losers of this Evergrande mess. Trade War feels like a really old topic by now, but its very much alive and kicking. The whole de-globalisation feels like a long term new theme one could do investment after

It’s clear to my by now that China has decided to decrease the wealth gap created in the past 20 years. There has been some obvious losers, like education companies but a lot of companies have been hammered for various reasons. In my view even the Evergrande mess is part of this same theme (at least partly). What is less talked about is that there are also some winners in equalization. Just like in the US with stimulus checks which created a huge buying freenzy. If the poor in China got less poor thanks to wealth redistribution, perhaps the customer base of Vinda’s Tempo tissues grows from a few hundred million to half a billion? If a dedicate another posts to thoughts on China I would like to explore this are more. As always happy to hear you input, who do you think are the winners if China wealth gets more equally distributed?

It’s very good to be back posting, hope you got the tribute hints, man 30 years already!

A study of small caps listed on the Hong Kong exchange

Over the last couple of years much of my portfolio performance can be attributed to a few holdings which have 2-5x in a short period of time. The latest one being Modern Dental Group where the price recently just took off.

If you want to read my Modern Dental Group analysis just click here.

Discussing with other small cap value investors, investing in HK small caps can be a bit like tapping on the Heinz ketchup bottle. Stocks do nothing for years and then all return comes at once. I hadn’t really experienced it like that in the past but lately this resonates a lot with me. As you can see the price graph of Modern Dental above is was a grueling holding which went from 3 HKD down to just above 1 HKD. Consider that this happened in an environment where stock markets where extremely bullish. Then suddenly the stock just pops fantastic when it happens. I want to explore what drives these sudden burst of returns. How to catch them, how to act when they break out and also try to identify if and when its time to either reduce or sell your position. This is Part 1 which focuses mainly on how to catch these type of holdings.

Catching the Rocket

The very first step of enjoying the returns of a small cap that significantly re-rates is to actually be there when it happens. I have a number of stocks that I held and sold, just to see them sky-rocket later. Or stock that I held for a long time when they started to move upwards I was quick to sell and afterwards looking like a fool when the stock continued to double from my selling price. First step is to actually be there when the stock takes off. As we will see from a few examples of stock price graphs, its easier said than done.

Miserable failure

Modern Dental was a success example, let’s look at some failures as there is probably more to learn from those. For the ones of you that have been reading the blog from the very beginning, you might remember this:

Recently some of you readers have contacted me either through the blog or on twitter to discuss Essex Biotechnology. Since I also recently increased this to a high conviction position, I thought I would share my thoughts on why I did so and some very recent development.

To start with I want to say so far Essex has been a terrible investment, I allocated significant capital to Essex on 5th of April, very close to the market bottom. And the stock is trading flat since then, whereas my portfolio is up 54%, a pretty remarkable underperformance. Why am I then adding to this holding which obviously the market doesn’t really see any value in? Well the (maybe obvious) answer is that I believe that the market is wrong and that there is significant upside in Essex to hopefully be unlocked. The most exiting trigger is that Essex today posted what I have been waiting for for some time now.

The Board is pleased to announce that, as informed by Mitotech, the topline data of VISTA-2 will be released and presented on 24 February 2021 after trading hours, and an announcement will be made by the Company accordingly

This post won’t be very structured but I would just comment on different aspects of the company. Let’s jump in