I promised in my “Summary 2022” to comment on the holdings that contributed most positively/negatively in 2022, they happen all to be Hong Kong stocks and among my largest positions.

Best stocks in 2022 – PAX Global and Vinda

Worst stocks in 2022 – Modern Dental & Greatview Aseptic

All four stocks have been reduced somewhat to raise cash during Jan/Feb but they are still high to fairly high conviction position. So without further ado let’s jump into discussing these for stocks. (click read more for a mega post)

+ Strong core business of dental prosthetic production with good cash flow generation. Possible margin improvement after factory move in 2019/2020.

+ Although listed in HK, this company mostly has stable revenue from developed markets – Europe/USA/Australia.

+ A kicker is the growth opportunity in China where the need for dental care is huge as well as the high fragmentation in the market.

+ Debt tenor recently extended, which shows prudence of liquidity management.

+ Low valuation with good potential for turn-around and multiple expansion if management can integrate acquisitions successfully.

– So far acquisitions has just grown top line, nothing has feed through to the bottom line. Markets are currently in doubt of management execution on the investments.

– Strange history of running core operations on land where the lessor did not have the right to lease out the land (might have been hard to understand beforehand though).

– Recently started a share buy-back program (about 1% of float so far), although this is general is an acceptable way to shift out earnings to shareholders, it more looks like a way to prop up the share. The management should concentrate their efforts and cash in improving the businesses they bought.

Background

Modern Dental Group (hence forth called MDG) is the only listed company in the previously described segment of prosthetic producers and distributors. The company floated on the Hong Kong exchange in December 2015, offering 175m new shares and 75m secondary shares at 4.2 HKD. This brought in about 660m HKD cash to the company. The current market cap of MDG is 1.2bn HKD.

The company started growing significantly during the early 2000’s with centralized production facilities in Shenzhen, China, for dental prosthetics production. The company used third-party distributors to sell their low prices dental prosthetics. This co-operation grew over the years to a large number of distributors world-wide, selling their products to local dentists. The offshoring of prosthetic production to China has seen strong growth (as discussed in Part 2) and created good cash flow for MDG. This enabled the company to bit by bit acquire it’s distributors and smaller local labs. MDG has through acquiring these companies become a direct distributors to the dental clinics with the purpose to control the whole mid-stream segment. The goal as I interpret it, is to be able to provide a full-service offering, both low cost options from China and the higher quality products from the local labs.

As we learned in previous posts, the development of CAD/CAM technology enables the local labs (who can afford it) to fight off the low cost production in China. With machines doing most of the work, low labor cost is not as big of an advantage as in the past. This is probably the main reason MDG has been on a spending spree over the last 5 years. My guess is that MDG see the next leg of growth as consolidating the small local dental labs into bigger units where economies of scale works better with CAD/CAM. In fact MDG has already created such labs of larger scale in Hong Kong, Melbourne and Emmerich (close to the border of Netherlands). By consolidating the market MDG might be able to out-compete smaller local players.

Ownership structure

47.4% of the company is held by the Chan family

16.1% of the company is held by the Ngai family

The rest 36.5% is free float.

A family majority owner is very common in HK listed company. This is both a blessing and a curse, if it’s the right family leading the company, it could be very good with a strong owner to lead company. HK also has many cases where this has gone totally wrong and money is more or less embezzled into other non listed entities which are family controlled. Given the nature of the business in this case and that two separate families are large owners, I see this risk as minimal. It’s rather the risk of incompetent leadership which would be the largest risk. At the same time, the families have all the motivation in the world to not mis-manage their company, since they are more heavily invested than anyone else. On balance in this case I see it as a positive that this company has a strong family owner.

Fundamentals Overview

The core of this company has been the large production facilities in Shenzhen China, they have delivered solid cash-flow (some 150m HKD per year back in 2014) and continues to do so. Although exactly how much is not fully visible anymore, since income is now mixed together with all the acquisitions done (more on that later). The company has some 780m HKD in debt, which recently has been refinanced (at a cost) at a longer tenor (5 years). Being prudent and taking up longer term financing, even if it costs more, I see as a positive and responsible management. I would not want to see debt levels escalate, now at 2.45x EBITDA.

As we can see above, Europe is the largest market, followed by the U.S. Unfortunately profit contribution and margins per region is not available, but from my readings Europe together with Hong Kong (included in Greater China) are the two regions which contributes most to the bottom line.

Revenue and Net Income

Top-line has increased significantly (mainly from acquisition) but so far small effect on bottom line. One reason is that a loss making US operations was added into 2017 figures. Maybe it will be famous last words, but my investment thesis here is that we are experiencing the worst right now. On the flip side there is a lot of potential for margin improvements, if management delivers in terms of synergies and operations of scale in general and for the U.S in particular. Another factor for margin improvements, will be few years down the line, when the move to the new factories in Dongguan are completed.

P/E contraction

Given the declining share price and flat Net Income, the P/E has just kept contracting, reaching as I see it, attractive levels.

Acquisitions Overview

Given the large number of acquisitions this becomes an important component to poke a bit deeper into. The below tables summarizes the acquisitions over the past 5 years.

Larger Acquisitions

Smaller acquisitions (dental labs)

In total since 2013 MDG has done acquisitions to the tune of 1.2bn HKD, the current market cap of MDG is 1.29bn HKD, adding on net debt of about 450m HKD, the Enterprise Value of MDG is 1.75bn HKD. For MDG to currently be fairly valued they must have grossly overpaid for the companies the bought. Or the market has miss-priced the company and its significantly undervalued.

Has MDG in general overpaid?

The short answer is, probably yes. The slightly longer answer is, the earlier acquisitions seems to be OK-ish. Its hard to judge exactly how improvements and synergies are moving along per region and contributing to the bottom line. The jury is still out on the execution of their strategy of lab purchase RTFP (MicroDental) being the main one. Just looking at the purchase prices of the larger acquisitions, the market price seems to be around 1x Revenue of the companies, which without any deeper insight, sounds fairly cheap. The problem child in my view is RTFP, which is bleeding pretty badly.

One case where the company was somewhat unlucky was the SCDL acquisition in Australia/New Zealand. Australia’s government changed the contributions to dental healthcare, which has reduced the business significantly overall in Australia. The market is slowly recovering from this.

A look at RTFP Dental (MicroDental)

This acquisition in 2016 is quite different from the larger ones done in the past. First, this is the only large scale dental lab acquisition done. Second, this is the first significantly loss making operation bought. As you can see in the second table above, MDG has also started to selectively buy Dental Labs in other places of the world, but that has been small scale compared to this huge acquisition of 21 labs in one go. MDG acknowledged that RTFP was losing a lot of money, US$-9.3m which translates to -73m HKD (that is a lot for MDG which has a historical Net Income of about twice that).

These were their main rational why this still made sense to acquire:

Brand Name – MicroDental is a renowed brand in USA.

Customer network – Platform for MDG to further penetrate the USA market, mainly through the 21 labs around USA.

Laboratory EBITDA – at US$5.9m EBITDA on lab level shows there is actual value in the company. RTFP is burdened with high admin costs, an expensive facility in Dublin etc. MDG believed it could improve results through offshore product lines, elimination of unnecessary corporate expenses, reductions in rent and operating expenses for the facility in Dublin and streamlining measures.

Location of dental labs of RTFP Dental

Tax benefits – MDG can enjoy tax deductions through amortization of goodwill, to the tune of US$7-9m.

Finance cost – 2016 US$2.4m of the losses were due to Finance costs and MDG would be able to fund this more cheaply.

The Latest comment released last month on MicroDental business outlook:

“The North American market has experienced a slight drop in sales (of less than 2%) and a drop in sales Volume (less than 3%) due to (i) the management’s focus and attention on the ongoing restructuring and integration of MicroDental during the period as a result of the temporary distortions arose from closure of inefficient locations and relocation of production facilities during the period; and (ii) the management’s planned decision to focus on higher priced and margin products and gradually phase out the lower priced and margin products in MicroDental Group.”

In the latest semi-annual report they disclose how the reshaping of the MicroDental business is progressing, in total it contributed -9m HKD in loss for the first half of the year. Still terrible, but much better than the 73m HKD loss before. This progress will be key to MDG’s long term success and potential share price recovery. I think it will be hard to come out of this and create shareholder value, meaning turning this business highly profitable. So far the market agrees with me and I think this the main reasons why the stock is down -60% since the acquisition was announced. This of course give us that invest now, a good discount. So the damage done by this acquisition is in my view already reflected in the share price, now there is upside if they actually manage to turn it around properly. There are some early signs that they are making good progress.

The strange land story

Going through the IPO documents a very strange story emerges. The very short version is something like this: The factories MDG are running in China are rented by some type of local community in the suburbs of Shenzhen. This was all well for many years, until Shenzhen grew so much that the land became more valuable. The city has after that re-evaluated the claims different people or groups have to that land. It happens so that Shenzhen government has realized that this local community does not have the legal rights to this land and therefore MDG ends up in a very strange position. Basically MDG could at any point be evicted from the land (with a grace period for moving out). Since this local community of course strongly opposed the Shenzhen governments view on the matter, this has ended up in some type of legal conflict. Consequently MDG decided, it’s time to start to look for a new factory in neighboring Dongguan. This also makes sense from a labor cost perspective, since Shenzhen starts to become a bit too developed and rich. Back in the IPO days, 2016, there was still a long runway until a new factory would be up and running. I can’t understand how investors would be willing to bare this big risk of being thrown out of their factory, before the new one is finished. Now this issue is diminishing, the first phase of the constructions of the new factory is scheduled to finish end of this year. Even if MDG was told to start to prepare to move out by tomorrow, the impact would not be terrible. I would not have been comfortable to invest in MDG earlier than now, just by this fact. These kind of issues is not something I contemplated for my other investments, you always learn something new and the number of traps in emerging markets are so much greater.

Valuation

Being the only listed company in it’s segment of course makes valuation from a peer perspective more challenging. What MDG themselves paid for the acquisitions is one guideline of the value of the business. Currently the Enterprise Value of MDG is about 1.75bn HKD with revenue of 2.28bn HKD for rolling last 12 months. On the very simple metric of paying 1x revenue, the stock is undervalued by some 30%. I don’t suggest this to be a very good method though, I prefer to look at cash flows.

As we have seen in Part 1/2, the dental business is not very cyclical and has a nice growth trajectory in many parts of the world. These are important reasons, since it gives stability to revenues and income. The big question for the valuation is, what will be happen with the margins? The company has gone from stable 14% Net Income margins in 2012, down to around 6% in the past years. Will that improve, become even worse, or stay stable going forward? This all depends on how well the company manages all the acquisitions done over the past 5 years, since they brought down the margins.

Assumptions:

For revenues I do not assume further large acquisitions, just some minor labs being bought. Majority of revenue growth is assumed to be organic growth. China as we have seen is growing very quickly and that will also feed through in the companies revenue growth. The growth rates are 2%, 4% and 6% per year.

My base case assumptions is that some type of efficiencies of scale will start to take effect. Also that the bleeding stops in the U.S. dental labs turn into a profit, there is a few percentage points of margin improvement just from that. Making the base case in my view, fairly conservative.

WACC = 12%, given the stable nature of the business with revenue from developed markets I think a lower WACC is warranted. 12% maybe is not even low enough. I would go even lower, if it wasn’t for that I wanted to keep some risk premium for the uncertainty around management execution.

This gives me my three valuations:

Base = 1.42 HKD per share (I give this a 60% weight)

Bull = 2.19 HKD per share (I give this a 30% weight, since I see it as more likely that margins will improve)

Bear = 0.53 HKD per share (I give this a 10% weight, I see it as unlikely that margins would further significantly deteriorate)

Which in turn gives me a weighted target price of 1.56 HKD per share and about 20% upside to the current share price.

Summary

I have been somewhat torn if this is a good enough case to invest in or not. I do love a good turn-around (maybe I like them a bit too much). It’s not easy to catch the bottom and this stock is currently a slow falling knife. 20% upside at a WACC of 12% is not extremely good, but a DCF is also tricky. I’m not a slave to the DCF and there is a lot about this company not captured in my simple DCF. Just changing the assumptions a little bit moves the valuation up and down by quite a bit. For example a WACC of 10% instead of 12% gives a Base case valuation of 1.86 HKD per share.

I like that the family is so heavily invested in this company, they must have a great understanding of the dental industry. They are executing on a strategy they believe will be fruitful in the long run and there are some early signs that the losses in USA are coming to an end.

I think what made me finally decide is the defensive nature of this business. There is a reason this company initially traded at a P/E of 30 and most healthcare and dental related companies are trading at very high multiples. So buying this below a P/E of 10, is pretty darn good for a defensive business.

I initiate this at a 4% position as a Long Term Holding in my portfolio, I will not increase my position before I see proof of margin improvements. I’m willing to give the company about 1-1.5 year to prove that they can improve margins from here.

In this second post we will start to understand more of the dental supply chain and it’s players. The below picture borrowed from a Modern Dental Group presentation, gives a nice overview of the different market players. This pictures also reveals the major investable industry players:

The focus in Part 1 was on total industry level, revenue and all the different services provided by a dentist. There are a handful of listed dental clinic companies globally and some of them are listed in the picture above. Singapore listed Q&M has an interesting spin-off that I might come back to, but for now I find the other segments more interesting. The next layer in the supply chain are the laboratories and distributors. There is only one listed company in this layer of the supply chain, Modern Dental Group. It has been listed about 2 years now on the Hong Kong stock exchange.

How are dental prosthetics made

There are many different services at a dentist, the more simple ones being just a filling. But when you need a prosthetic of some kind, you enter into a more complex product supply chain, with companies supporting the dentist. This is what we will learn more about now.

Before we dig into more detail we non-dental experts need some more background info first. It’s a pretty complex production flow to replace or repair teeth, I found videos like the ones I linked below very helpful to understand the process and turn-around time to produce any type of dental prosthetics. This is what makes it so fun to be an investor. On the journey to find new investments, you get to learn so many new things. I really had no idea about these processes a few months ago!

I had several sector themes in the past and some of them are still in my portfolio (EV’s, breweries, funeral). My most well covered theme has been Electric Vehicles. It’s time to learn about a new niche segment of the market. Over the past year I have spent a lot of time looking in to many different Pharma/Biotech/Healthcare related companies. Unfortunately it has not yielded in anything I can confidently hold long term. I thought I had an investment case with Teva, which I spent a lot of time researching (Teva – The Perfect Storm in 2 parts) but at the later stages of my analysis I decided not to. The main reason why I in general have such a hard time pulling the trigger on a Health related investment, has been the research pipelines. These Phase I, II & III research pipelines often drives most of the value in these companies. I just feel I never have an edge, in understanding the probability, if a product is going to pass through these stages. In the search for something more understandable but still healthcare related, I ended up with dental care. Although still complex, I think this is a niche which is understandable and therefore for me – more investable.

Some segments and markets in the dental services industry has very attractive investment dynamics. First of all it’s generally very defensive, especially in countries where dental care is government sponsored or part of a health insurance. Second, is demographics and economics, the world is getting older and we also live longer combined with increasing wealth. Old people need dentures and implants, and reaching a certain level of wealth, you start to take care of your teeth in another way. These two factors create a significant long term tailwind for these products. Third, it is a very fragmented market, with custom made products. This creates a very low price transparency for the end customer, it will take a long time before end consumers have proper price comparison, for dental services. In many cases it’s also not needed, given government sponsorship or insurance covering the procedures.

This will be a multi part exploration in understanding the dental sector and the investable players in that space. If any of you readers happens to be a dentist or just have deep knowledge in the sector, please do help out over the coming posts to explain the dynamics of the industry.

The Big Picture

It is very hard to get a good global industry overview. First of all because of scarcity of data, secondly because different sources group different products and services in different ways. I have done my best to pull together a industry overview from a number of sources. Most of the industry data is from 2014-2015.

One can divide everything related to mouth health into two main segments, my focus will be on the first of these two:

Dental Services – All products and services when you visit the dentist (teeth check-up, tooth filling, dental implants, cosmetic changes, xray, etc).

Oral Care products – All products and services outside the dental clinic (toothbrush, toothpaste, dental floss, mouthwash, etc). Although a large market, I will leave this segment for now, this series will focus on Dental Services.

Tooth decay (dental caries) is the most widespread chronic disease worldwide and constitutes a major global public health challenge. It is the most common childhood disease, but it affects people of all ages throughout their lifetime. Current data show that untreated decay of permanent teeth has a global prevalence of over 40 percent for all ages combined and is the most prevalent condition out of 291 diseases included in the Global Burden of Disease Study. Another very common disease is periodontitis, which means inflammation of the gums and supporting structure of the teeth. Periodontitis starts with gingivitis, where the first sign is bleeding from the gums. I think many of you have experienced early stages of this, when you are flossing your teeth and the gums start bleeding.

We can also see that teeth is a question of economic background, as people get richer they eat more sugary food and get more tooth decay. But as income rises, more of those teeth gets fixed:

The U.S. dental services is today a market of more than a 130bn USD. The European dental market is valued at above 80bn USD. The U.S. dental market is growing at an average growth rate of 5.8% per year since the 1990’s. The European Dental market is a more mixed picture, but on average it is growing at a slower pace of 1-2%. For the Asian region the data is much more scarce. Large countries like China and India has not come nearly as far as the highly developed countries, but growing at significantly higher pace (from low levels).

The below picture gives a feeling for when markets are saturated in terms of number of dentist per 1000 population. One can see a pattern of about 0.5-0.8 dentists in developed markets, whereas a country as China has significant growth ahead:

Dental Services explained

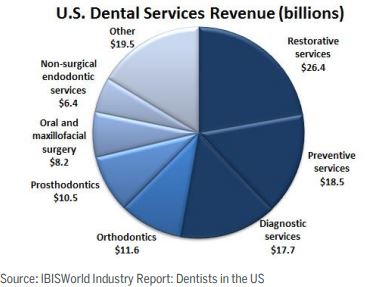

To explain the different parts of the industry I use this split from 2015 on the U.S. Dental Services:

This gives a brief explanation of these different sub segments of dental services

Restorative – Dental fillings, dental crowns, procedures treating damaged or decaying teeth or gums.

Preventive – Routine dental exams, cleanings, fluoride and sealant applications.

Diagnostic – Digital radiography and x-rays, etc.

Orthodontics – Treating improper bites and misaligned teeth.

Prosthodontics – Artificial teeth, partial or full dentures, bridges and implants. This also includes veneers, a thin layer placed over a tooth and other types of tooth restoration.

Oral surgery – reconstructive surgery, jaw alignment, dental extraction. This segment also include cosmetic surgery to the jaw.

Endodontic – Root canal procedures and other treatments related to the pulp of the tooth.

Other – Includes services to dental practices, distributors, software solutions, HR, marketing, financial planning etc.

Within all these areas the are a number of large to medium sized companies providing different products and solutions to the dental clinics. In coming posts I will dive into some of these segments and see what kind of investment opportunities we can find.

Highly Fragmented Market

Dental centers do not normally belong to large chains or a company group. The dental service industry is in fact highly fragmented, with smaller dental shops run by one or a few dentists. The top four dental service firms in the US account for less than 2% of domestic market share, and over 88% of the US dental service companies operate with less than three dentists, according to a IBISWorld Dentist report. The same situation is seen globally in most countries. Some exceptions are: China, where some 350 dental practices control over 50% of the market. This is due to most current centers are government run, in a similar way as hospitals. But as could be seen in the above picture, China is a very under-served market in terms of number of dentists overall. The growth currently seen in China is coming from smaller groups of private centers. In Europe the situation is also mostly of a fragmented market (with Finland perhaps being the exception):

This fragmentation seems to have been something the Private Equity firm have picked up on. Obviously there are synergies to be had by running a larger operation. So from a very fragmented market we have seen the early days of some consolidation. This article (Pan-European dentistry is here, but at what price?) though argues that some players have been overpaying.

This fragmentation in dental clinics has also meant that the bargain power has been sitting with the dental suppliers. These companies are huge in comparison to the small dental clinics and supply the clinics with all the products they need, to run a modern dental clinic. Given this fragmentation on the dental clinics side, most of the investable universe is with these companies supplying the dentist with their products.

Your mouth is expensive

A strong motivational factor for spending on dental care is of course just pure looks. To change the appearance by moving misaligned teeth, using veeners, or just a simple whitening. This is a fast growing segment in the market, where products like Invisalign has grown tremendously. These procedures though are like cosmetic surgery, a luxury product, which will cost you a lot. The Invisalign procedure will cost you anything between US$4000 – Us$8000.

Very few people in the world can afford to out-of-pocket front the full bill for dental care when more advanced procedures are needed. Replacing a lost tooth with a single implant will cost you between US$2000-$6000 depending on where you are in the world. Since dental issues, like a lost tooth seldom is an emergency, we end up with a lot of untreated cases. Because of the high prices, the dental market is to a large extent driven by the level of government support. Few countries has totally free dental care to the whole population though. A rich country like Australia for example seems to have a very lively debate on this, where even young people go with untreated tooth decay: The dental divide – and the decay of public dental services.

Countries like northern Europe which are famous for their welfare states, have free dental care for kids up to around 18 years of age. Even in these countries adults have to pay, although there is still usually some type of back-stop coverage from the state. For example in Sweden 50% is covered between 3000-15 000 SEK and 85% of the amount above 15 000 SEK is covered by the state. This kind of coverage is similar to expensive health insurances in other countries which include dental. For example the health insurance I myself have (global coverage), covers 80% of my dental bills. Even if this sharing of cost helps, people still need to pay out of pocket fairly significant amounts when doing a larger change, like implants or dentures.

So the growth of dental care is very much up to governments willingness to pick up the bill. The other factor is is increasing overall wealth, like in China, where a rising middle-class is deciding to start to pay themselves, either out-of-pocket, or through better health insurances. To reach a larger part of the population, price is obviously an important factor, if companies are able to lower prices, volume will follow.

End of Part 1

I hope this set the stage for a series of posts on dental related companies. Do you have any investment favorites in this market segment and why? Anything you would like to add in terms of important industry trends? Please leave a comment!