A very quick post, just to register my portfolio changes:

Adding Mix Telematics – 4% position

After a lot of searching I found a new investment interesting enough to take a small position here the day before the quarterly report is out. The company is Mix Telematics, which is dual listed in South Africa and the U.S., ticker MIXT in the U.S. I have been following this company for quite a while, but waited to invest given the fairly high valuation in the past. This has come down now and I find the valuation a bit to attractive to stand outside when they are going to release their quarterly figures. There are risks, as always, a large part of revenue is derived from South Africa, the currency being the big issue here. Also some exposure to Brazil, where a larger competitor has had some troubles lately. But the company seems to hit off on a lot of my investment criteria: Customers seems happy with their products and customer retention is good, owner led, expanding in USA after the owner moved there to grow the business. Long track record of growth. Fantastic capital allocation, doing large buybacks when the shares were undervalued a few years back. Seems to overall be a high quality company. At a later point I will try to do a full write up, in the meantime, if you want to do your own DD, feel free to comment and we can discuss!

The valuation has really run ahead of the company now, I’m not selling my full holding, because I want to be long term in this holding. But I need to stay somewhat true to my principles of not being too exposed to companies that has taken a lot of future potential growth upfront in the share price. I’m sure there will be future buying opportunities to add back to this position if the company continues to deliver.

Something a bit odd happened recently with my holding Tonly Electronics. Due to re-structuring in the company which is the majority shareholder in Tonly, the HK exchange forced TCL to make a bid for the shares in Tonly. Since this was an involuntary bid, the bid premium was very small to non-existent. I had not to planned to sell my shares in this bid, since the company intended to let the company be listed. But over the last weeks it seems a lot of shares have turned over just around the bid price and I’m afraid the free-float will be so significantly reduced that this already illiquid company will be virtually impossible to trade in. Given this and that there are many other China related companies with attractive valuations I decided to sell my full holding as of close Friday. This was a very unusual sell for me, given that I think I’m selling my shares too cheaply, but given the strange circumstances I don’t want to get stuck holding these shares.

This increases my already pretty large cash buffer, so I choose to add to two of my holdings:

Dairy Farm – I’m bringing this back up to a 6% weight in my portfolio. I sold some of my shares at 9 USD and now I get to buy then back at below 6 USD. I’m expecting a terrible report given the situation in Hong Kong. This is truly a buying, when there is blood on the streets, investments. Go back to my old full analysis if you want to understand the company better. For example Dairy Farm’s holding in Yonghui Superstores is worth almost 3 USD per share. So you are getting large parts of this company for free right now. The HK situation does not look good, but I still think this is a buying opportunity.

LiveChat – Also bringing this to a 6% position. Have been experimenting with their sales process, which did not end up satisfactory according to the companies latest update. Nevertheless the company continued to grow the number of customers, which is impressive. I’m very interested to see the next set of financials, if we can see some early signs of increased revenue per customer. I think they might be getting there.

As i already hinted in my previous post, NetEase is the only company left that I identified as not having an “edge” against the market. I was at the time of posting not willing to sell it just yet, but now the time has come. I was looking for a better exit level as well as rumors around NetEase selling its e-commerce business. The rumors have now come true and the stock has since rebounded significantly, which gives me the opportunity to exit this holding at a decent level. NetEase has been the holding I traded the most of all my holdings. The reason for that is probably the extremely high volatility of the share. Calculating the return on an investment is actually not the easiest thing when you bought, sold and re-bought the stock over these years. My trades summarized since I started this blog:

41 shares in my starting portfolio at US$147.84 per share.

May 2016: Bought 15 shares @ US$166.08, August 2016: Sold 17 shares @ US$213.33, September 2016: Sold 19 shares @ US$231.27, October 2016: Sold 20 shares @ US$248.6

I then held no shares until, May 2017: Bought 23 shares @ US$276.76, May 2018: Bought 24 shares @ US$233.35, As of Friday: Sold 47 shares @ 278.81

On an initial investment of some 6061 USD, I have made a total return of 5578 USD through all these transactions. Even if this company has been one of my better investments, as my investment philosophy develops, I need to stay true to what I think will generate out-performance in the long term. Owning one of the worlds largest gaming companies does not really tick those boxes for me any-longer. This is a company fully understood by the market and do not have any longer term view than the market. Rather I might see more problems ahead than the market does, the game production space has become an awfully crowded space. To keep delivering hit games, just gets harder and harder. It therefor feels quite comfortable parting with this holding.

Coslight Technology

This holding has truly stayed in my portfolio from day 1 and never left the portfolio, it’s one of only two holdings that’s been with me from the start (the other being Sbanken). So it’s a bit depressing that Coslight is one of my worst investments since I started the blog. I did sell some shares back in September 2016, when the stock was up over 100% from my bought price. I then increased in Coslight again at a lower price. This did reduce my total losses on a dollar basis. Of a US$6000 initial investment, I lost some US$2681 over these 3.5 years. Nevertheless a huge detractor to performance, since my overall portfolio is up some 59% since inception.

Lesson learned

From most bad investments you usually take away some expensive learning, some stocks teach you more than others though. The big lesson in Coslight for me was – company debt. When I started the blog one of my big “bets” were around Electric Vehicles and how they would take over the car industry. I made quite many bets in this sector and the ones that are left are Coslight and LG Chem, which are battery cell manufacturers. I think my predictions from back then has more or less come true in terms of EV adaption, something that was definitely not clear to everyone at the time. What I did fail to realize was how costly it would be to create next generation battery cells. Quite frankly money that Coslight could not muster, given how indebted the company already was. This has really been the main problem for Coslight, they did not have the financial muscles to create the next gen battery cells. Instead they ended up selling parts of their largest factory to pay down debt and kind of give up on the EV cell race. It’s always easy with hindsight, but I should have sold this earlier. I had understood more than a year ago that this was the case, but it was a bit of pride and stubbornness from my side to keep holding. I’m selling this company now when it was trading at a very low multiple. But again, taking into account the debt, the company is actually not that cheap on an Enterprise Value basis. So this is my lesson, I learned to put much more emphasis on cash-flow generation versus debt and Enterprise Value. Something that feels very obvious to me now, but something I managed to get wrong when I was excited about investing in a small cap EV-theme related stock 3.5 years ago. Debt can be a blessing when things are going well, but it might also wipe you out when it doesn’t.

2019 has been the toughest year for the GlobalStockPicking portfolio in terms of under-performing against the MSCI World benchmark, YTD the return stand at 3% vs 15% for MSCI World. I did very well up until about April this year, when I posted about a new all time high for the portfolio. Such boasting was immediately punished with severe under-performance. Both US and European markets have performed well, whereas Asia is more in line with my portfolio. With quite a lot of Asia exposure the portfolio has fallen behind, but even taken that into account I have under-performed.

Obviously I’m disappointed, but more so I have been scratching my head. Is this how it should look like at a market peak, as irrational investors pile into Beyond Meat like investments and rational investors fall behind? Or am I on the wrong track and investing in poor value trap companies etc? Before going further into that topic, below is the return in a more digestible format:

Two portfolio “issues”

First “issue”, I’m sitting on a few Hong Kong small cap investments which are pretty much dead in the water. The market sentiment in Hong Kong currently is not very good and although my companies (thinking foremost of Tonly Electronics, Modern Dental Group and Dream International) seem to have little exposure to trade tariffs (for Dream it’s actually a positive) or exposure to Hong Kong protests, the stocks are not moving. These three holdings at 17% of my portfolio seem to be pretty much in value trap land at the moment. Sure they might be cheap, but there is no interest in the market to price these stocks at higher multiples. So is this an issue then? Well yes and no, if it’s important to keep measuring yourself against a benchmark which keeps moving upwards, then it is an issue. If you are long-term and the underlying businesses are doing all right, it’s a non-issue, at some point the market will wake up and revalue the companies. Given that I want to be very long term, I have decided that this is not an issue for me. Obviously that might change when the semi-annuals soon are released for this companies.

I’m having too many large cap companies in my portfolio where I have no reasonable edge against the market. Not having an edge on the market is something I thought a lot about lately and something I realized is critical for long term out-performance. I see two main cases (there might be others) where I think I could still have an edge in large caps:

That I have a much longer investment horizon than the market (my investment in Diageo, Inditex,, Essity, Dairy Farm and LG Chem are based on this).

Irrational selling flows in certain market segments, for example Hong Kong listed stocks right now, or stocks not fitting into the ESG portfolios which seems to go into everything right now (my investments in Swedish Match, BATS and Philip Morris are based on this).

Basically this gives me a few large cap holdings which have not really been bought with these “edges” in mind: NetEase, Gilead Science and partly NagaCorp. But NagaCorp being a Cambodian investment, listed in Hong Kong and after a big run-up trades around 6bn USD in MCAP. I would say it’s not really a main stream large cap investment just yet.

Portfolio Changes

Selling Gilead Science

Already back when I invested in Gilead I “confessed” that I had struggled to find a really great Pharma investment case. I relied heavily on other investors and their analysis when I invested in Gilead (Another Portfolio change Aug 2017). I think shows a bit how my investment style has changed since then. Today I would not do such an investment without doing my own due diligence a bit deeper first. Given the “no edge” argument, it’s time to let this one go and invest in something where I think I found an undervalued company, which the whole market is not aware of.

Selling British American Tobacco (BATS)

I might be right that ESG tilts in portfolios have put tobacco stocks on the no-go list of investments, but I can’t just base such a large portion of my portfolio just on this. I need to see that these companies long term are capable of delivering great returns in my portfolio. Swedish Match I think qualifies there, that’s why I increased my position there. Philip Morris might qualify long term, I do like the IQOS product and long term it’s success will be pretty crucial for delivering really strong shareholder returns. In BATS case, I’m pretty confident that this is a good defensive company which will deliver decent shareholder returns, if I was a corporate bond investor I would like BATS quite a lot. But I’m looking for slightly higher returns and I gambled a bit too much on this ESG angle having 3 tobacco companies in the portfolio, two is enough and BATS is the weakest link.

Selling Essity and switching into it’s subsidiary Vinda

This switch is something I haven’t mentioned, but looked at for a long time now. Vinda being a Chinese tissue paper products producer, majority owned by Essity and listed in Hong Kong. Basically the case is that given demographics, Vinda will see much stronger growth than the rest of Essity, which is also confirmed in historical results. So all else equal given higher growth Vinda should trade at a higher multiple, but it’s rather trading just in line with Essity. Why? Probably because Vinda being somewhat illiquid in comparison with a small float of some 25% on 2.2bn USD MCAP. But you get a Swedish governance run company, with full exposure to China’s growing middle-class and elderly population. This is truly something to put in the long term bucket.

Some pictures showing how Essity and Vinda traded since Essity got listed as a separate entity (spun out from SCA):

I was unfortunately asleep at the wheel during the summer when the spread was at it’s largest. The spread shrunk after great H1 results from Vinda, but has increased again on back of Hong Kong stocks under-performing in general (probably due to protests etc). So this gave me another opportunity to switch into Vinda.

Initiate new position in AK Medical Holdings

Another twitter inspired holding (LiveChat being the other), which I feel a bit ashamed of not having found myself (given how much time I spend looking for stocks on the HK exchange). Again my timing here is not the best given that the stock has rallied quite a lot recently. A full write-up will have to wait, but this is the holding I hinted at in my 3-D printing post. The company produces orthopedic implants, mainly for the hip and knees. The sell their products almost exclusively in China. Over the last few years the spent quite a lot of resources to use 3D-printing technology to create better custom made hip implants. Just as I wrote about in the 3D-printing post, the most successful examples of 3D-printing so far has been for the human body, where the need for customization is high. The companies sales of 3D-printed implant parts is still fairly small compared to total revenue, but it’s growing very nicely. It also shows the companies ambition to not just be the low cost option for implants compared to international players.

I think the company partly have traded so strong lately due to trade war speculation. If the trade war intensifies, probably international companies selling hip implants will face difficulties, which could favor a local player like AK Medical. My investment thesis is not based on this though, although of course it’s nice to have a trade war hedge in the portfolio.

This company is not trading at very cheap levels, so I will start with a fairly small position. You will have to wait a while longer for a full write-up.

Sizing and adding in Sbanken

I sell the full holdings in Gilead Science, BATS and Essity as of close Friday. This takes my cash level to about 14.1%. Of this I allocate a 5% to Vinda and a 3% position to AK Medical Holdings. Of the cash left I decided to increase my position in Sbanken again, which has traded down significantly on general Nordic bank stock weakness. I take my Sbanken position back to 5% of the portfolio, leaving a small cash buffer.

+ SaaS company with strong track-record of growth in number of customers, revenue and cash flow.

+ Providing services in a niche with strong tailwinds, companies need to find way to communicate with their customers online effectively.

+ Founder led with large shareholding from the founding team.

+ Operating out of Polish University city, young entrepreneurial city, with low staff costs.

+ Has invested in developing value adding services like ChatBot and Helpdesk, these are also sold as separate services.

+ Potential upside (if approved) in Polish preferential taxation of income generated by intellectual property rights.

+ / – Somewhat questionable that cash flow is shifted out as dividends instead of reinvested in such a nicely growing business. Current dividend yield is ~6%, which of course is attractive and it also significantly reduces risk that there is anything fraudulent going on in the company. It is after trading in Poland, a market I’m not so familiar with.

– Growth in number of customers have been on a downward trend.

– Competition increasing, both from freemium services and larger player with a wider offering.

– Reporting comes first in Polish which later is translated into English and some info only released in Polish (I thank google translate).

Background and Overview

The company has one prime product and three “add-on” services which also can be bought separately. As can be seen in the timeline above, the three add on services are fairly new products.

LiveChat which is the main product of the company is a software used by businesses to communicate with customers browsing their website. They see the product as a simple chat window placed on the website. The business owner and his agents, on the other hand, have access to the sophisticated application designed for communication and quick customers service. The company operates its products through a SaaS (Software as a Service) model. Examples of the product’s use are very varied. LiveChat solution can facilitate sales processes in e-commerce, serve as a recruitment supporting tool in education and HR and as a contact channel in industries which require personalized communications, such as real estate.

Knowledge Base platform lets companies create their own knowledge bases, which can be accessed by both their employees and clients

ChatBot is a product which allows the creation of conversational chatbots to handle various business scenarios. Their main goal is to automate corporate communications and to improve the effectiveness of customer service teams by addressing repeatable customer inquiries. The solution, introduced to the market, fits into the Company’s strategy to develop the offering of products for text-based customer communications. At the same time it responds to the now popular trend towards automation of communications using AI-based mechanisms

HelpDesk solution enables customers to leave a message for a company by using dedicated email addresses. It’s also possible for team members to create a ticket if a customer’s query came from other communication channels, such as LiveChat, Facebook Messenger, WhatsApp or a phone call.

Management

The supervisory board seems to be a mix of company founders who are no longer active in the company and board professionals . The two founders who are still active are:

CEO – Mariusz Cieply has been with LiveChat since its founding in 2002 – first as software developer, later as project manager and now as its CEO. Mariusz is one of the main shareholders of LiveChat.

CFO – Urszula Jarzębowska has been working in LiveChat Software from 2002. She has 12 years of financial experience with both public and venture-backed companies.

Ownership Structure

The ownership proportions within the consortium which holds 47.1% is the following:

Marius Cieply (CEO) 15.57%, Maciej Jarzębowski 11.69% (who is a founder and (I guess) married to the companies current CFO), Jakub Sitarz 11.69% (Founder/programmer no longer active in the daily business of the company). The remaining ~8% of the consortium is not disclosed, but the CFO has a portion of that.

Business & Outlook

The company has a very impressive list of customers

The growth in number of paying customers can be shown in many ways, this is LiveChat’s own presentation:

Another way to describe this would be the following:

I think this gives a clearer picture of how customer growth has been on a steady downward trend for some time now. But it’s also quite clear in the MoM graph that it seems to have bottomed out, at least temporarily. Another aspect to this is the churn of customers, which LiveChat is not as generous with data on. But they do disclose that the churn has been stable around 3%. They also note that the leave ratio is much lower for larger customers (companies using the more expensive subscription plans and buying more licences).

We will come to competition soon, but obviously the customer growth is affected by strong competition which has entered the space. Livechat has previously been spoiled to with very little effort gain large traction, today they have to work harder. One channel they use are affiliate partners who get a kick-back for redirecting paying customers to LiveChat. I think you understand what kind of affiliates that is, you google for “best customer chat service” and you land on different homepages ranking providers, all with links to the providers. Overall LiveChat does not invest huge amounts of money trying to win customers, but is rather trying to use clever cheap ways. Like providing a very good blog/homepage of their services. This is if I grasped the competition correctly is more in line with how the freemium services/companies are acquiring customers. So judging from figures there seem to be a potential turn-around or at least flattening of a previous “nasty” trend, the stock market seems to think so too.

A big positive is the fantastic margins that LiveChat has historically held, which enabled the large dividend payments. It’s just a staggering generating such cash flows at the same time as the company has had yearly growth in the 20-40% range.

I think Poland instead of Silicon Valley is a big reason for this, wage levels are probably 20% of the Valley, but the quality of staff is definitely not 20%. In many ways it could be better, given this being one of few very attractive employers in the city. Historically many great companies were built in slightly off locations with staff that wanted to live there.

Outlook

It’s undisputed by now, how businesses and consumers are moving online, the clothing industry being one of the ones most affected by this. Another example could be retail banking, which used to be a very personalized face to face experience. Today most people want to avoid visiting a bank branch. Overall all companies today have a challenge in communicating with their customers. This has obviously spurred growth in multiple new channels where companies tries to find new ways to connect with their customers. LiveChat has been riding on that wave and I think it’s a wave that still has a lot of runway left, giving this investment idea a nice tailwind. On the other hand the LiveChat growth figures are telling a story of slowing growth, that I account more to competition than that the actual market itself has entered a lower growth stage. According to the available market data and the company’s own estimates, the current value of the market for live chat type solutions may exceed USD 700m, with LiveChat having some USD 35m of that.

Zendesk has a nice graph showing how new ways of interacting with companies comes naturally for younger generations:

The market got a scare a few years ago, believing Facebook and Apple wanting to step into this space in a bigger way. Facebook would make it possible for customers to chat with companies on their homepage through Facebook messenger. Given that Facebook messenger is a well established channel it would not be strange that more and more companies moved more of their customer communication to that channel. LiveChat’s comment on this is: The company is developing a business ecosystem around its products, LiveChat and Chatbot, in order to be able to better address users’ needs. Thanks to these developments, they will be able to communicate with their clients via multiple platforms, not just using their website, but also via text message, Apple products, mobile devices, Facebook Messenger, social media communicators and platforms. For the interested reader a longer comment from around that time: LiveChat comments on Facebook chat.

Group’s growth strategy

This is taken from the company presentation:

The company’s development strategy is based on making continuous, balanced investments into further development of the LiveChat product, including in particular: a) functional development of the app; b) new communications channels;

• development of the ticket system

• mobile systems;

• social media;

• an integrated communications tool c) data-driven tools for larger corporations

Much of the above is based on the new services like Helpdesk, which recently launched. Overall LiveChat is mimicking much of what the market leader Zendesk is doing, which leads us into the Competition. I also learned from reading around on their blog that they have deployed clever tactics in the past to improve their LiveChat product. The company used a stand alone service called chat.io to play around and test new functionality without disturbing existing user-base. When a lot of new ideas had developed within the chat.io product, they merged them into the new LiveChat 3.0 version and started to roll it out to existing customers (Blog reference)

Competition

In interviews the CEO states that they are not afraid to charge properly for their product. It’s a premium product and they do not go for free versions (except a short free trial), since their experience is that it’s hard to convert a non-paying customer into a paying one. So they are confident they have a product which stand out in the competition. What does the landscape then look like in such a niche as chat-related services on company homepages?

I will focus on the two companies larger than LiveChat (tawk.to & Zendesk), which are at two extremes in their strategy of offering this product.

Tawk.to

Visiting their homepage the first message is: “You never have to pay for live chat software again”. This is the largest freemium service of chat. Given it’s free it’s not surprising they have a huge number of customers, 2.2 million. As we know today, free always comes at a cost, like usage of customer data. There are also some other costs, like a monthly fee if you want to remove the tawk.to logo from the chat. Also they sell services of agents that talk in your chat for US$1 an hour. This obviously attracts a big set of smaller companies without the budget shelving out every month for a chat system and perhaps do not even have the staff to man such a chat. It is on one hand worrisome that such an attractive product is offered as a freemium/fully free service. On the other hand, as long as LiveChat can offer something significantly better, these companies might be door-openers to new customers. Tawk.to is not the only provider of such a freemium service, some of the smaller players in the above picture follow the same strategy. At the other end of the spectrum we have:

Zendesk

Zendesk is a US listed company with 10bn USD in Market Cap. They come from a different background, having customer support as their main product and later adding on chat. Another difference is that the company did not organically grow these new product offerings, but bought several companies. For example the Chat functionality was bought from Singapore based Zopim. Later they also acquired BIME Analytics which became their data analytics (BI-tool) platform. Zendesk currently have some 145 000 paying customers for all their products and some 45 000 chat paying customers. The company has expected revenues of some 181m USD the previous quarter, so they clearly charge their customers. Just focusing on the chat side of Zendesk, the pricing levels are very similar to LiveChat.

When you start to look into Zendesk and seeing the changes LiveChat done over the past few years, one realizes that they are playing catch-up on services Zendesk has already launched. In LiveChat’s investor presentation they mention that Helpdesk is to challenge Zendesk and other competitors with an attractive alternative. This product was just launched in May 2019, so it’s to early to tell how it has been received. Also in their presentation they compare number of paying chat customers for Zendesk vs themselves. Zendesk has over the last year lost customers each quarter, whereas LiveChat is (as you have seen) still adds customers.

Here it’s worthwhile to stop for a second, just how much is a Zendesk customer paying? (181million*4)/145000 = 4993 USD per year, per paying customer. Given that a lot of that revenue is not chat related, it still shows the income potential per customer with a wider offering (which LiveChat is building up currently).

Here I have plotted the trend in how much an average LiveChat customer is paying:

Although the slope of the trend is not extremely strong, I’m still happy to see that this is a positive trend. It tells quite a lot, that while the market has been flooded with good freemium options that LiveChat has increased income per customer. This is such an important point and one of the main reasons I see LiveChat as investable. Some observations around this:

LiveChat is now building up their product offering, with cross selling there is potential to reach closer to Zendesk earnings per customer.

LiveChat has been able to historically, at least slightly, up-sell their products to each customer (meaning more agents per customer, or adding chatbot services etc).

LiveChat is still adding paying customers, when Zendesk (with their strong overall offering is losing paying customers).

Capital Allocation

The company paid out almost 100% of profits during 2018 and during previous years paid out a large portion of profits as dividends. Over the last six years the company has paid out some 200 million PLN or 55m USD to shareholders (current market cap ~220m USD). My guess is that this was partly done because the founders wants to “cash out” without selling their shares and losing the company. So since the company was growing so nicely without massively reinvesting profits, they reasoned that they could shift out profits through dividends. In my view this has been a mistake, looking at how Zendesk has reinvested all of its cash-flow (and then some) they have grown much stronger over these years. If they can reinvest the capital at a higher rate of return than what investors can find elsewhere that should be preferred. At the same time Zendesk runs a totally different model of acquiring companies for growth. Whereas LiveChat grows organically with a strong local Polish team, which is a model I prefer. They have increased number of staff from some 84 to 145 in 1.5 year, so it’s not LiveChat is not investing at all. Many of these people are deployed to work on the chatbot if I have understood things correctly from my communication with the company. They also bought the domains chatbot.com and helpdesk.com last summer. So clearly they are stepping up things and deploying some of that nice cash flow back into growing the business.

But it’s still a fact that the company is paying out a very high dividend, currently at a 6% yield. So here I am complaining that you get a 6% dividend yield owning the company. Well, repeating myself, I think the ROI had been even better if they managed to deploy that capital for further growth. So given that LiveChat do continue to shift out capital to it’s investors and probably will not see the same high growth numbers as Zendesk, is the company worth buying?

Valuation

Maybe we should deal with this question directly. Zendesk seems to be the market leader, why don’t I just buy that company if I like this niche? Short answer, because it generates losses and is at nosebleed valuation levels. I do think Zendesk is an impressive company, but for an investor like me, who cares about valuation, it’s a no go. A quick comparison table:

LiveChat

Zendesk

EV/Sales

7.2

14.2

EV/Gross Profit

8.6

20.3

EV/EBITDA

10.7

Negative

EV/Free CF

15.5

248.0

So with that out of the way, let’s move over to trying to value LiveChat.

Valuation inputs:

Equity Risk Premium: Being a company listed in Poland I would normally warrant a higher risk premium, but given that all revenue is generated in USD from customers worldwide and the high dividend yield basically putting the accounting fraud risk at zero I’m going to go with my standard rate of 10% discount rate.

Growth: As we have seen, customer acquisition growth has stopped around 10% lately, whereas revenue growth has been somewhat stronger than that. My assumption here is that customer growth rate probably over time will drop to low single digits, but the growth will rather come from up-selling to existing customers.

Revenue Growth Bull: 20% first 5 years, dropping to 10% over the coming 5 years

Revenue Growth Base: 10% for the coming 10 years.

Revenue Growth Bear: Dropping to 5% over the first 5 years and then 0% growth.

Margins: Track-record is fantastic and I see no major reason that this should deteriorate significantly.

Margin Bull: 65% EBITDA margin, increasing to 68% over the next 5 years.

Margin Base: 65% EBITDA margin constant over time.

Margin Bear: 65% EBITDA margin, decreasing to 60% over the next 5 years.

Taxation: Here I have left the tax rate in all scenarios at the current corporate tax rate. But there is a kicker in all scenarios that the tax rate would drop under a new legislation interpretation where intellectual property revenues could be taxed at a much lower rate (IP Box tax)

Valuation Bull: 74 PLN per share – Probability 20%

Valuation Base: 48 PLN per share – Probability 50%

Valuation Bear: 30 PLN per share – Probability 30%

Which gives me a weighted target price of: 47.8 PLN per share, in line with my base case valuation. With the share currently trading at 33 PLN, I see enough upside (45%) with limited downside to enter a position at these levels. I will start with a position which is 4% of my portfolio and see how this develops.

Key Metrics to follow

This will be something I want to introduce for all of my holdings, some very brief key metrics that I will keep up to date, to follow the company over time.

LiveChat Key metrics:

Month over Month Added customers.

Quarterly Revenue per Customer.

Changes in capital allocation strategy.

Excess Cash Adding to Swedish Match and Irisity

The excess cash I have left after buying into LiveChat I distribute equally to my positions in Swedish Match and Irisity. Both companies in my view have a very nice risk/reward profile from here. Swedish Match Zyn product seem to be doing great and I don’t understand why the share is trading so weak when the Swedish Krona is losing even more to the USD lately. Irisity is reporting Q2 results soon and it will be interesting to see how the roll-out of their products to security companies have been going.

The Gartner hype cycle in the picture above can be used in many situations in life. For example I would draw a very similar curve of my perceived knowledge of equity investing. Starting at a low level back in 2002-2003 as a total beginner. Quickly I reached a peak of disillusion around 2007, when all my investments had done great for 4 straight years. I was master of investing and yearly returns of +30% seemed likely. Like another famous expression, do not mistake a bull market for actual investing skills. In early 2009, all my illusions had been shattered and quite a lot of my bank roll as well. From there onward I have been a more humble investor, knowing how little I actually know about investing. Humbly crawling up thew slope of enlightenment is a fun exercise and what this blog is about. Maybe you have gone through a similar cycle?

But enough about our investment psyches, let’s talk 3D-printing.

3D printing and the hype cycle

As probably most of you are aware, we had a big hype in 3D printing a number of years ago, where do you think we are now on the above Gartner curve?

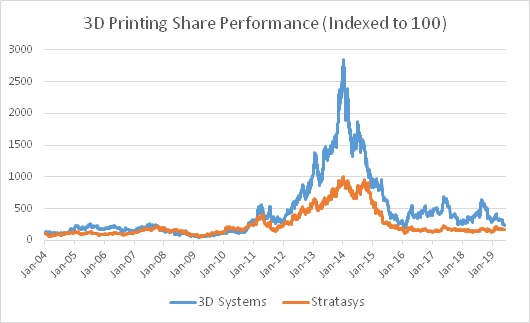

Let’s look at the share-price performance of two of the largest pure-play 3D printing companies.

It looks like a long term shareholder got a very wild ride above, but most likely no returns so far. And its clearly a boom-and-bust hype cycle we have seen in 3D-printing. But as with every hype, there is usually quite a lot true business opportunities hidden behind all the hype. There are numerous examples of investments that after a hype has died become very profitable. Probably the most famous examples are all after the IT-bubble burst, picking up the survivors like Amazon would have been a good decision. A less famous example would be the extreme hype we had around Clean-tech up until 2008. Since it coincided with the Lehman collapse it’s perhaps slightly less obvious. But winners did emerge here also, like Vestas Wind, which bottomed in 2013 and has from that bottom reached back to around pre crisis all time highs, giving bottom fishers a return of about 17X their money.

To believe that there is something real underlying in a hype, one has to read up on the use cases of 3D printing. And I have to say, the more I read, the more I realize this is actually all around us already and it’s not going to get smaller.

Obviously there is no telling where we are in the cycle, but I would put 3D printing right now somewhere at the earlier part of “slope of enlightenment”. But then thinking about it in more detail, is it really relevant to put everything under one 3D printing label? Probably not, Gartner actually splits up the universe of 3D-printing and maps out all sub-segments onto the curve:

As you can see the graph above is almost 1 year old. So if Gartner is spot-on on all these observations, everything should now be shifted 1 year ahead on the curve. I find the light blue dots especially interesting, since that indicates technology being some 2-5 years from reaching a mature stage. Some of my first question seeing the above graph was, how big is this industry? And are there any examples of a mature 3D printing business? Let’s look at those two questions:

It’s seems to be a very healthy growing industry: “3D printing (including hardware, materials, software, and services) will be $13.8 billion in 2019, an increase of 21.2% over 2018. By 2022, IDC expects worldwide spending to be nearly $22.7 billion with a five-year compound annual growth rate (CAGR) of 19.1%.”

Examples of 3D printing businesses

The first and most cited example where 3D printing has taken over the industry completely is hearing aids. According to this article, already in 2017 hearing aids produced in the western world where all literally 3D printed: Phonak 3d printed hearing aid. I find that fascinating, that one large hearing aid player (Sonova) moved to 3D print and within years the whole industry moved to it.

The next example is a tangent to my previous posts about the dental industry. The dental industry has multiple examples of 3D printing or “milling” machines that create custom made products for the mouth. But I think the most telling example is Align Technology, who were able to revolutionize the experience of teeth correction, with it’s invisalign products. Sometimes a video says more than a thousand words:

The third area of 3D printing is not where the technology entirely taken over or redefined it’s product area, but rather high tech production, where 3D printing is a superior technology to save weight, create complex shapes, etc. Again a famous example are the 3D printed parts that started to go into airplanes: Boing Dreamliner with 3D printed parts

Conclusions

So the more I researched and thought about 3D printing, I found 3 broad categories of 3D-printing services/companies:

Creating something unique with a custom fit being the selling point. Most often in someway related to the human body.

Creating a better performing product, by either creating shapes impossible to otherwise produce, with the aim the to increase performance, weight savings, etc.

Software products, machines and 3D printing base material/ingredients.

When talking the 3D printing hype, much of the focus has been on category number 3. But so far, almost all of the actual value creation has been in category 1-2. Align Technology being the shining star example. If you invested in ALGN at 3D Systems share price peak in Aug 2014, you would have returned 460% by now. With that knowledge, probably a good area to search for new investment cases would be in new such 3D printing disruptions and not the 3D printing machine makers themselves. On the other hand, if we are seeing a bottoming of these companies, maybe the also have decent upside from here on. I will be back with at least one investment case in this area in the not too far future.

A good friend of mine, who is the one I bounce ideas the most with, asked if it was possible to do a guest post. Without this guest, my discussions and investment ideas over these years would not have been the same. So I’m very happy to present some Macro thoughts from my friend – the first guest poster!

Has the US debt cycle come to an end?

Until this week, the equity market has been holding up fairly well despite the trade war, slowing demand in China and Brexit. But there is something on the horizon that suggests we should sell

equities and wait for a better entry point – the debt cycle in the US seems to have come to an end. A rate cut from the FED during the second half of 2019 would confirm that theory and should be a negative catalyst for equities.

I’m sure many of you have read and heard about Ray Dalio, founder and co-CIO of Bridgewater, one of the largest hedge funds in the world. He describes how the “economic machine works” through the debt cycle. Simply described; both companies and households spending consist of two factors; Income and Credit. Income tends to be fairly stable, growing a few percentage points per year, and is the base of a households´ and companies spending. Credit on the other hand tends to vary over time, perhaps you use credit to buy a new, larger house, or a new car while a company might use it to expand manufacturing capacity. Thus spending can increase faster than income by using credit.

A person’s spending is another person’s income – an important aspect in a debt cycle. This means if you are using credit to consume, another person’s income will increase. With increased income the second person can increase their credit thereby expanding their spending power. This chain of events can continue for years, until the debt cycle stops i.e. when households and companies stop expanding their borrowing. As the cycle turns and less is being spent due to lower credit growth, it means another person’s income is falling. That person will therefore not be able not borrow as much since their income is falling thus decreasing their spending power. The chain of events goes both ways creating the debt cycle. You will find a great summary of Ray Dalio’s theory of How the Economic Machine works here:

I’ve thought a lot about this and tried to quantify the debt cycle with the help of the 3m US treasury yield. We start with the simple assumption that if the demand for credit is high, the price of credit i.e. the interest rate, will rise. When demand for credit slows the interest rate goes down. The reason I’m looking at the 3 month yield is that it says a lot more about the credit demand right now compared to for instance the 10 year yield which factors in a lot of expectations about future inflation and economic growth.

By looking at the y-o-y change in the 3m UST yields we can see how the demand for credit has changed over the last year. This is what we typically do when looking at a company`s specific data, we compare the order book, revenue and EBIT with the same quarter last year to see if it’s gotten better or worse. The chart below tells us that the 3m UST yields are about 50bps higher than a year ago, meaning demand for credit has gone up.

S&P500 vs 3m UST y-o-y (bps)

US Corporate Debt growth y-o-y (%) vs 3m UST y-o-y (bps)

A general thinking when looking at Capital Goods companies is that when the second derivative in organic order growth turns negative it’s usually a good time to sell the stock. It tells us demand is about to stabilize i.e. order growth will go towards 0%. In the same way a positive second derivative, when organic order intake is negative, would be seen as a sign that order growth is about to

improve.

Applying the same methodology on the 3m UST yields a negative second derivative would tell us that the demand for credit is slowing, a strong indicator the debt cycle is coming to an end. The y-o-y change in the 3m UST started to stabilize by mid 2018 and has recently started to go down as a result of the lack of rate hikes from the FED. The Fed Funds futures market indicates we will have at least one cut from the FED during the second half of 2019 and another one in 2020. A cut in interest rates from the FED in the second half of 2019 would confirm the end of the debt cycle which would mean the start of a bear market.

FED FUNDS Future Aug19-Dec19

S&P500 vs 3m UST y-o-y (bps) including a rate cut in October

When investing in a company I do my best to understand the products the company is selling. I want to understand the environment the company is operating in, competitors, brand value, together putting the company into a context. I try to understand the management of the company and where they want to take the business. I then try to look long-term if the industry has headwinds or tailwinds and how much sales is affected by the general market cycle. All this and more goes into my valuation of the company. But even when I try to cover all bases, the stock market keeps throwing curve balls left and right, I had my fair share and there will certainly be more in the future. The other day it felt like I was dealt another curve ball.

The management of Edgewell Personal care, went out bought a shaving company start-up called Harry’s for 1.37bn USD. Edgewell with an Operating Income of some 300m USD, net debt of 1.1bn USD and Market Cap (pre announcement) of some 2bn USD, thought it is in a good position buying a start-up for 1.37bn USD. Worse than that, they pay 1.085bn USD in cash and very little in stock. This brings debt levels to seriously tough territory, at a time when I at least believe we are close to the peak of the cycle. I thought I bought a low risk defensive company, it suddenly transformed into a equity position sitting on a huge debt rocket.

Harry’s is one of the competitors (Dollar Shave Club being the other) that I mentioned i my analysis of Edgewell when I invested. They are taking market-share from Edgewell, Gilette and BIC over the last years, particularly in USA. Harry’s top-line revenue is expected to be about 325m USD in 2019 (growing at 30% historically).

They do own their factories and it has been an impressive growth case, so of course it isn’t a worthless investment, it’s just a combination of overpaying and overstretching Edgewell’s balance sheet. I’m so disappointing in Edgewell throwing in the towel to create this themselves organically. By acquiring Harry’s it’s like admitting to not being able to compete with these guys. That speaks volumes to me about the management of Edgewell. At today’s close, I sell my full holding in Edgewell. Obviously I wish I never invested in the first place, given that I now take a -16% loss on the holding, but I never saw this coming. Investments really can surprise you in so many ways..

Other thoughts about my holdings and the market

Markets have come off a few percent from their highs and my portfolio has under-performed quite a lot the last few weeks. Some of that poor performance obviously is related to Edgewell, but there have been other holdings performing poorly too. Trade war is a big worry, especially for my portfolio that feels fairly exposed to this. I’m not very positive on us seeing a deal anytime soon, there is too much pride in China for that. At the same time I changed my mind about the so often cited coming China crash. I still think it will come, just not this year. My bets are on a pretty ugly 2020 in China, with serious deterioration in their economy in the later part of next year. These things are impossible to predict, but from everything I read and hear, it seems like we have already passed the peak. It will just take a while for slow moving things like the property market to start to wobble and finally fall.

My more defensive companies like Philip Morris, BATS, Swedish Match, Diageo, Dairy Farm, Gilead, Inditex and Essity has not really done that much lately. They have more or less performed in line with the market or slightly better. Below I instead focus on the more high risk holdings:

Tonly Electronics

One of my largest holdings, the quite illiquid company Tonly Electronics has traded down. This is quite warranted given the Trade War that to some extend will affect the company. I’m still hopeful that the company will be able to improve margins during this year, which really is the key thing to be watching in the next report for the first half year. The fairly good dividend yield, which was paid out yesterday, at about 5% yield is also reassuring. Tonly was an opportunistic investment where I see a very deep value case, but not necessarily something I want to hold for another 5 years, as long as some of that value is unlocked at some point.

Nagacorp

A holding that has been a long term holding, but where I numerous times discussed if it really should be. Nagacorp came through with how they plan to finance the third stage of their expansion in Cambodia. After reviewing the terms, I actually think they are quite fair this time. So I decided to increase my position size here and for now throw away my doubts and really firmly put this in my long term holding bucket. I increase my position size to a 7% holding, nearly doubling the position size, more or less back to where it was before I started to reducing my holding. Somewhat ironically the average selling price of my shares is exactly where the shares are trading at now, 8.96 HKD per share. But the situation was different then, I very much doubted that the majority owner would come through with a decent deal for everyone. Now that he did, it changes a lot for me. I many times stated I would be happy to have a very large holding here if I just could trust management. The trust gauge is not really at 100% yet, but it’s much higher than before and this money printing machine feels like a stable holding at 7% weight.

Coslight Technology

One of my original holdings since I started the blog. As explored the Electric Vehicle theme back 2015-2016 most signs pointed to that the real S-curve effect would start around 2020. I remember telling colleagues back in 2015, isn’t it cool that in just 5 years all big car companies most likely will be launching full EV line-ups. That more or less have come true, maybe with a 1 year delay until we really see them in every car dealership. Even if I got the EV theme correct, the company Coslight has not turned out as I planned when I invested more than 3 years ago. Now when EV sales numbers really are starting to climb, I don’t think its the right time to sell this company. I’m down significantly, on not really any news. The company still also has its game software development which is a profitable cash generating business. There is a lot debt here as well, which has been my main oversight when investing. So I might get wiped out from the debt, but somewhat stubbornly perhaps, I want to see this through.

Irisity

Finally my speculative holding Irisity has lately been on a bit of a roller coaster ride. But fundamentally on the company, I’m even more bullish than before. First quarter sales on Monthly Recurring Revenue was fairly solid showing continued strong growth (from low levels). The latest news about HikVision also being banned, just like Huawei, plays perfectly in the hands of companies like Irisity. The largest competitors in this space for sure are the Chinese, with companies like Sensetime having huge software development teams on video-surveillance. If western companies avoid or even are banned from using Chinese tech in this area, a lot of the competition in the market is removed. I’m considering to increase my holding further, but will stay put for now and hope I can increase and a better entry level.

That is all for now. I’m trying to find time to publish a real deep analysis of some new ideas I have had for some time now. But you will have to wait a little bit longer for that. Comments as always are appreciated!

The portfolio reached a new all time high on Friday last week. It’s not very long ago I wrote a post where I shared my thoughts around the market. I thought then that we had started a cyclical downturn and the bear market had started. Suddenly the market feels stronger than ever again. My gut is telling me to sell everything and run nowadays (my gut is always early). Well I will just continue to pick stocks and do my best to outperform, whatever the markets generally decides to do. That being said, with the sell of Cheetah Mobile and now UR-Energy, I am lifting cash levels again, making the portfolio more defensive, at least for a short while.

My portfolio as of Friday last week:

UR-Energy

So why am I selling my full holding as of close today? I didn’t even come around to write a post about this, as I probably earlier promised to do. First of all, this was a speculative holding, just as Cheetah Mobile. Second, the spot Uranium price really is stubborn. Even though so many fundamentals says its bound to go up long term, it continues to stay at rock bottom levels. A holding like UR-Energy then becomes like a far out of the money call option, which is bleeding time value as I’m waiting. Now I believe the stock has moved up only for the petition they have sent in, that USA should secure some yellow cake production from North America, and not rely on places like Kazakhstan for the supply of uranium to it’s power-plants (and perhaps nuclear weapons). So, maybe this will go through – I honestly have no idea. If that happens, there is probably much more upside here, but I have no clue to guess the chance that this petition is accepted. Also that was kind of a kicker in my investment case, not what I built my speculation on. My investment case was built on, that the world would wake up to nuclear and how much we really need it. To meet climate goals and as base power source when moving more to wind and solar. But no, it does not seem to happen at the speed/pace I was hoping for. Lastly I have some new upcoming investment cases that I will present in due course, I need the cash for this/these investments. I’m happy to take some money of the table here, netting a 10% gain on this speculative position.